Introduction

India was the first country in the world to make Corporate Social Responsibility a statutory obligation for large companies. Section 135 of the Companies Act 2013, operational from 1 April 2014, requires qualifying companies to spend at least 2 per cent of their average net profits on specified social-development activities. For the UPSC aspirant, Corporate Social Responsibility is a compact case study that sits at the intersection of GS3 economy, GS2 governance, and the ethics paper, because it tests how the state uses corporate law to channel private resources into public goods.

This note explains how the Section 135 regime works, the Schedule VII menu of eligible activities, the role of the Ministry of Corporate Affairs in supervision, the link with corporate tax treatment, and the main criticisms after a decade of implementation. Data cited is drawn from the Ministry’s National CSR Portal, the National CSR Exchange Portal, and IBEF snapshots through financial year 2024.

Quick Facts at a Glance

| Parameter | Detail |

|---|---|

| Legal anchor | Section 135 of the Companies Act 2013 |

| Effective from | 1 April 2014 |

| Rules | Companies (CSR Policy) Rules 2014, amended 2021 |

| Applicability threshold | Net worth of Rs. 500 crore, OR turnover of Rs. 1,000 crore, OR net profit of Rs. 5 crore |

| Mandatory spend | 2 per cent of average net profit of preceding 3 years |

| Oversight | Ministry of Corporate Affairs (MCA) |

| Reporting portal | National CSR Portal and MCA-21 |

| Schedule | Schedule VII lists eligible activities |

| CSR spend FY2023 | Rs. 29,987 crore (around 17,000 companies) |

| Tax treatment | CSR expenditure not deductible under Section 37(1) of Income Tax Act 1961 |

| Penalty regime | Civil, 2 per cent unspent to Unspent CSR Account |

Background and Historical Context

The intellectual roots of CSR in India pre-date the Companies Act. The Gandhian idea of trusteeship, the Tata Group’s hospital and university endowments, and the Birla family’s temple and education projects had long anchored a voluntary tradition of philanthropy. The first formal policy articulation came in 2009 when the Ministry of Corporate Affairs released the Voluntary Guidelines on CSR, drawing on OECD and United Nations Global Compact principles.

The 2008 global financial crisis, the Satyam accounting scandal of the same year, and growing concern about jobless-growth distribution nudged the Parliamentary Standing Committee on Finance to recommend a statutory CSR regime. The Companies Bill 2011 introduced Section 135 with a comply-or-explain framework, and the Companies Act 2013 translated this into law. When the Companies (CSR Policy) Rules came into force on 1 April 2014, India became the first country to legislate a minimum corporate social-development spend for qualifying companies.

The regime was further tightened by the Companies (Amendment) Act 2019 and the 2021 rule revisions. These shifted CSR from a soft comply-or-explain model to a hard mandate. Unspent amounts must now be transferred to an Unspent CSR Account or to funds listed in Schedule VII, such as the Prime Minister’s National Relief Fund or the Swachh Bharat Kosh, within specified timelines. Non-compliance is now a civil wrong with a graduated penalty, and every CSR project above Rs. 1 crore must be subject to an impact assessment by an independent agency.

Key Provisions of Section 135

Applicability Triggers

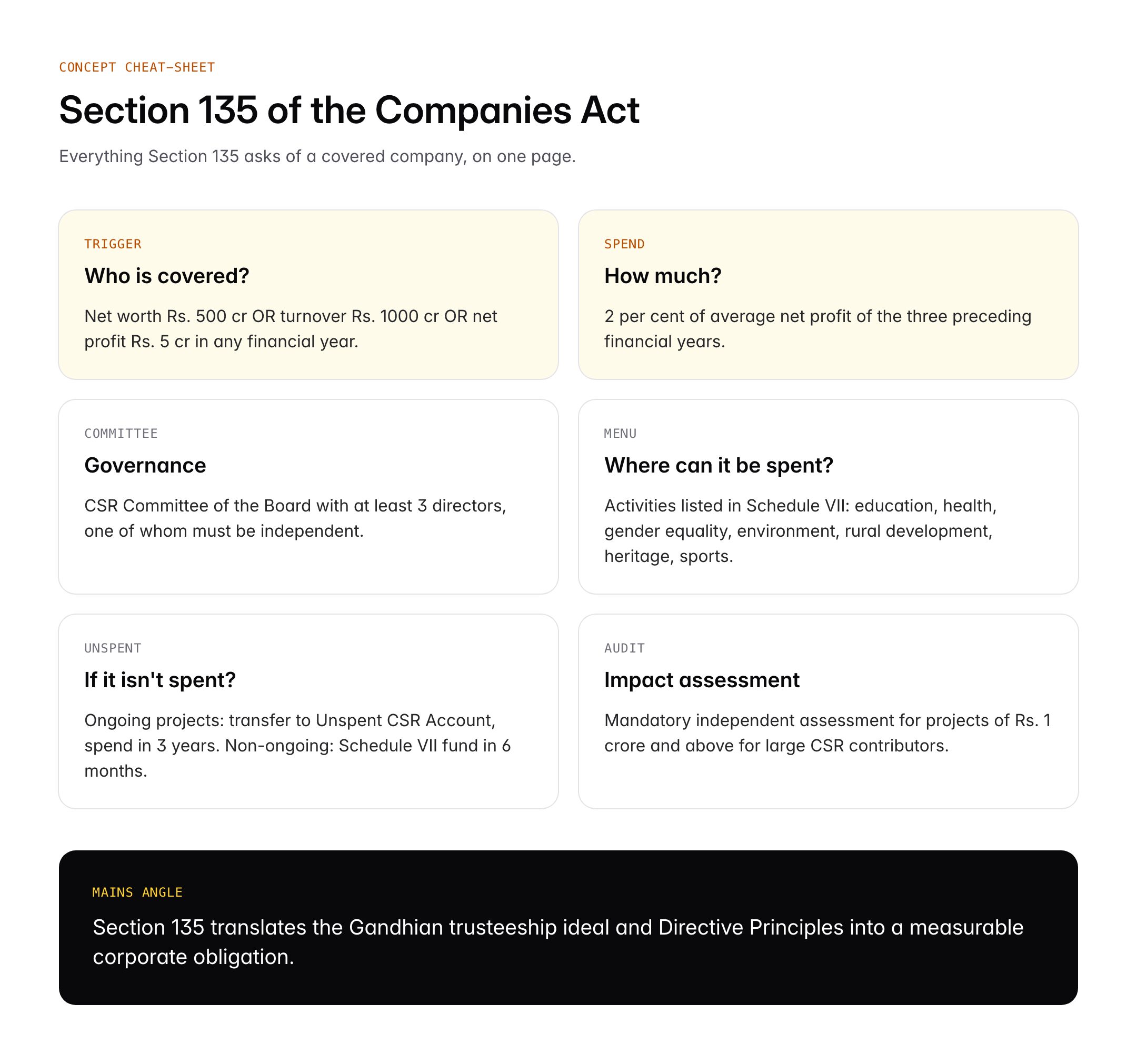

A company falls under Section 135 if, in any financial year, it crosses any one of three thresholds: net worth of Rs. 500 crore, turnover of Rs. 1,000 crore, or net profit of Rs. 5 crore. Once applicable, it must constitute a Corporate Social Responsibility Committee of the Board with at least three directors, one of whom must be independent.

Two Per Cent Rule

The covered company must spend, in every financial year, at least 2 per cent of the average net profits made during the three immediately preceding financial years. Net profit here is defined by Section 198, excluding profits from overseas branches and dividends received from other Indian companies already under CSR.

Board and Committee Roles

The CSR Committee formulates and recommends a CSR Policy indicating activities, budget and monitoring mechanism. The Board approves the policy, ensures activities are implemented, and discloses the CSR Policy and composition of the Committee on the company website in a prescribed format.

Schedule VII Menu

Eligible activities are listed in Schedule VII, which covers hunger and malnutrition, education, gender equality, environmental sustainability, protection of national heritage, measures for the benefit of armed-forces veterans, promotion of sports, contributions to PM National Relief Fund, the Clean Ganga Fund, slum development, rural-development projects and technology incubators at academic institutions. The Ministry expands Schedule VII by notification; disaster management and research on Covid-19 were added during the pandemic.

Unspent Amount Rule

Under the 2021 amendments, unspent CSR money for ongoing projects must be transferred within 30 days of the end of the financial year to an Unspent Corporate Social Responsibility Account, to be spent within three years. Unspent money tied to non-ongoing projects must go to a Schedule VII fund within six months.

Impact Assessment

For every project with outlay of Rs. 1 crore or more, companies with an average CSR obligation of Rs. 10 crore or more in the three preceding financial years must commission an independent impact assessment and place the report on their website.

Significance for UPSC and General Knowledge

- Operationalises Directive Principles under Articles 38 and 39 by redistributing private-sector resources.

- Illustrates regulatory innovation: the world’s first statutory CSR regime.

- Feeds GS3 topics on inclusive growth, Public-Private Partnership and fiscal federalism.

- Connects to GS4 ethics on corporate conscience, trusteeship and accountability.

- Provides hard data: Rs. 29,987 crore CSR spend in FY 2023, a useful Mains statistic.

- Interacts with corporate tax policy: CSR is not deductible under Section 37(1), which is a frequent Prelims twist.

Detailed Analysis: A Decade of Statutory CSR

Between financial year 2014-15 and financial year 2023-24, cumulative CSR spend by Indian companies crossed Rs. 2 lakh crore, according to Ministry of Corporate Affairs data aggregated on the National CSR Portal. Education and skill development alone accounted for roughly 34 per cent of total allocations, followed by health and nutrition at 27 per cent, and rural development at 13 per cent. The top five contributing companies in any given year typically include Reliance Industries, Tata Consultancy Services, HDFC Bank, Infosys and Indian Oil Corporation.

Geographic concentration remains a concern. Analysis by the NITI Aayog and a 2023 report by the India Development Review showed that Maharashtra, Gujarat, Karnataka and Tamil Nadu together attract more than 45 per cent of CSR money, while aspirational districts in Jharkhand, Bihar and the Northeast receive disproportionately less. The Ministry has responded by elevating aspirational-district-focused projects in Schedule VII and by setting up the National CSR Exchange Portal to match companies with projects in under-served regions.

Tax and fiscal implications are often tested in Prelims. CSR spend is not a business expense under Section 37(1) of the Income Tax Act 1961, so it cannot be deducted for computing taxable income. Some specific sub-categories, such as donations to the Clean Ganga Fund or the Prime Minister’s National Relief Fund, retain separate Section 80G deduction availability, creating a complex interaction that Mains essays should acknowledge.

The 2021 amendments also created an interface with environmental, social and governance reporting. Every listed company with a market capitalisation above the threshold set by the Securities and Exchange Board of India must file a Business Responsibility and Sustainability Report, and CSR disclosures are cross-referenced inside that filing. This has tightened the accountability loop between disclosure, spend and impact.

Comparative Perspective

| Jurisdiction | CSR approach | Mandatory spend | Disclosure |

|---|---|---|---|

| India | Statutory (Section 135) | 2 per cent of net profit | Mandatory BRSR + CSR report |

| UK | Voluntary, Companies Act 2006 | None | Strategic Report, TCFD |

| EU | Non-Financial Reporting Directive, CSRD from 2024 | None (spend), mandatory disclosure | CSRD, ESRS standards |

| USA | Largely voluntary | None | SEC climate disclosures |

| Indonesia | Limited statutory for natural-resource firms | Not quantified | Annual report |

| China | Voluntary guidance by SASAC | None | ESG guidelines |

India’s model is uniquely spend-mandating. Every other major economy compels disclosure but not expenditure. For Mains answers this permits a balanced evaluation: India gets higher expenditure certainty, but at the cost of a compliance mindset that sometimes treats CSR as a tax rather than a strategic investment.

Challenges and Criticisms

CSR in India has faced sustained critique on five fronts. First, box-ticking behaviour: civil-society research shows a significant share of CSR money is still routed to politically safe activities such as school infrastructure rather than rights-based outcomes. Second, geographic skew: Maharashtra, Gujarat and the southern states absorb the bulk of spend while aspirational districts remain under-served. Third, implementation agency capture: some companies channel funds through in-house foundations with limited independent audit; the Ministry’s 2021 rules tighten this but enforcement remains uneven.

Fourth, coercive philanthropy: scholars including Ajay Shankar and Arvind Virmani have argued that statutory CSR blurs the line between taxation and voluntary giving, distorting corporate decision-making. If CSR were fully tax-deductible, firms might spend more strategically; if it were replaced by a cess and pooled by government, impact could be more evenly distributed. The current middle path pleases nobody. Fifth, impact measurement: although the 2021 rules mandate impact assessment for projects above Rs. 1 crore, the methodology is not standardised, and comparability across assessments is limited.

Prelims Pointers

- Section 135 of the Companies Act 2013 mandates CSR in India from 1 April 2014.

- The applicability trigger is net worth Rs. 500 crore, OR turnover Rs. 1000 crore, OR net profit Rs. 5 crore.

- The mandatory spend is 2 per cent of the average net profit of the preceding three financial years.

- Schedule VII lists the eligible activities, amendable by MCA notification.

- The CSR Committee must have at least three directors, including one independent director.

- CSR expenditure is not deductible under Section 37(1) of the Income Tax Act 1961.

- Unspent amounts on ongoing projects go to the Unspent CSR Account for three years.

- Non-ongoing unspent funds transfer to a Schedule VII fund within six months.

- Impact assessment is mandatory for projects above Rs. 1 crore for large CSR contributors.

- Cumulative CSR spend crossed Rs. 2 lakh crore between FY 2014-15 and FY 2023-24.

- India was the first country to legislate mandatory CSR.

- The National CSR Portal is maintained by the Ministry of Corporate Affairs.

Mains Practice Questions

Q1. “Statutory CSR under Section 135 is a pioneering instrument but risks turning into coercive philanthropy.” Critically evaluate. (15 marks, 250 words)

- Outline Section 135 mechanics and Schedule VII.

- Present the case for statutory CSR: Rs. 2 lakh crore mobilised, aspirational-district focus.

- Present counter-critique: tax distortion, box-ticking, geographic skew.

- Suggest reform: standardised impact assessment, regional rebalancing, partial deductibility.

Q2. Discuss the role of Corporate Social Responsibility in achieving the Sustainable Development Goals in India. (10 marks, 150 words)

- Map Schedule VII activities to SDGs (health to SDG 3, education to SDG 4, water to SDG 6).

- Cite FY 2023 figures and BRSR disclosure to show integration.

- Flag gaps in monitoring and suggest National CSR Exchange Portal as a matchmaking tool.

Conclusion

A decade after Section 135 came into force, the verdict on India’s statutory CSR is mixed but mostly constructive. The regime has mobilised more than Rs. 2 lakh crore in development capital, institutionalised a CSR Committee inside thousands of boardrooms, and aligned corporate disclosure with the Business Responsibility and Sustainability Report. It has also, crucially, converted Gandhian trusteeship from a moral idea into a measurable statutory obligation, a quiet but important achievement in corporate-law history.

The next decade of reform must focus less on the rate of spend and more on the quality of outcomes. Standardised impact assessment, a stronger National CSR Exchange Portal to route capital into aspirational districts, and a narrowed gap between statutory CSR, Section 80G deductions and the forthcoming ESG disclosure architecture would push the regime from compliance to strategy. For UPSC aspirants, CSR is therefore not just a Section to memorise, it is an evolving story about how Indian capitalism and Indian democracy negotiate public purpose.

Frequently Asked Questions

What is Corporate Social Responsibility in India?

Corporate Social Responsibility in India is a statutory obligation under Section 135 of the Companies Act 2013. Qualifying companies must spend at least 2 per cent of the average net profit of the three preceding financial years on activities listed in Schedule VII, including education, health, gender equality, environment and rural development. India became the first country to legislate mandatory CSR when the rules took effect on 1 April 2014.

Why is Corporate Social Responsibility important for UPSC?

CSR is examinable across GS3 economy, GS2 governance and the GS4 ethics paper. It illustrates how corporate law channels private resources into public goods, it operationalises Directive Principles under Articles 38 and 39, and it provides a measurable Mains dataset of Rs. 29,987 crore spent in FY 2023 that can anchor answers on inclusive growth, ESG and Public-Private Partnership.

How is CSR related to corporate tax in India?

CSR expenditure is not deductible as a business expense under Section 37(1) of the Income Tax Act 1961. Specific sub-categories such as contributions to the Prime Minister’s National Relief Fund or the Clean Ganga Fund may remain eligible for Section 80G deduction. This non-deductibility is a frequent Prelims twist and distinguishes Indian statutory CSR from voluntary donations.

Which companies are covered under Section 135?

A company is covered if, in any financial year, it meets any one of three thresholds: net worth of Rs. 500 crore, turnover of Rs. 1000 crore, or net profit of Rs. 5 crore. Once covered, it must constitute a CSR Committee of the Board with at least three directors including one independent director, formulate a CSR Policy, and spend 2 per cent of average net profit annually.

What is listed in Schedule VII of the Companies Act?

Schedule VII is the menu of eligible CSR activities. It includes hunger and malnutrition, promoting education, gender equality, environmental sustainability, protection of national heritage, measures for armed-forces veterans, promotion of sports, contributions to the PM National Relief Fund, Clean Ganga Fund, slum and rural development, and technology incubators at academic institutions. The Ministry of Corporate Affairs can amend Schedule VII by notification.

What happens to unspent CSR money?

Under the Companies (Amendment) Act 2019 and 2021 rules, unspent CSR money for ongoing projects must be transferred within 30 days of the end of the financial year to an Unspent Corporate Social Responsibility Account, and spent within three years. Unspent money not tied to any ongoing project must be transferred to a Schedule VII fund within six months, otherwise graduated civil penalties apply.

How much do Indian companies spend on CSR?

According to Ministry of Corporate Affairs data, cumulative CSR spend between FY 2014-15 and FY 2023-24 crossed Rs. 2 lakh crore. In FY 2023 alone, roughly 17,000 covered companies spent about Rs. 29,987 crore. Education and skill development absorb around 34 per cent of spend, followed by health and nutrition at 27 per cent, and rural development at 13 per cent.

What are the main criticisms of India’s statutory CSR?

Five criticisms dominate. Box-ticking behaviour, with safe school-infrastructure projects over rights-based outcomes. Geographic skew, with Maharashtra, Gujarat and southern states attracting most funds. Implementation-agency capture by in-house foundations. Coercive philanthropy, blurring the line between giving and taxation. And weak, non-standardised impact assessment despite the 2021 rule mandating independent assessment for projects above Rs. 1 crore.