Introduction

When an aspirant searches for the NRLM SHG list, the query usually arises from a practical reason — verifying whether a village-level Self-Help Group is registered under the Deendayal Antyodaya Yojana National Rural Livelihoods Mission (DAY-NRLM), or studying the scheme for the UPSC Mains General Studies Paper 2 section on government interventions for vulnerable sections. The NRLM SHG database, hosted on the Ministry of Rural Development portal, is today one of the largest publicly accessible social-mobilisation datasets in the world, covering more than 100 million rural women organised into over 9 million Self-Help Groups across every state and union territory.

For the UPSC examination, the scheme matters far beyond the list itself. NRLM represents India’s flagship poverty-reduction architecture — a demand-driven model that organises the rural poor into community institutions, builds their financial literacy, channels credit at concessional rates, and progressively graduates them from subsistence to sustainable livelihoods. This article explains the features of NRLM, the structure of the SHG ecosystem, the bank-linkage programme, the on-ground impact documented by NITI Aayog and the World Bank, and the persistent challenges that the mission must still solve.

Quick Facts at a Glance

| Parameter | Detail |

|---|---|

| Scheme name | Deendayal Antyodaya Yojana — National Rural Livelihoods Mission (DAY-NRLM) |

| Launched | June 2011 (restructured from Swarnajayanti Gram Swarozgar Yojana) |

| Renamed | 29 March 2016 (as DAY-NRLM) |

| Nodal ministry | Ministry of Rural Development (MoRD), Government of India |

| Funding pattern | 60:40 Centre-State (90:10 for North-East and Himalayan states) |

| World Bank support | National Rural Livelihoods Project (NRLP), USD 1 billion IDA credit |

| SHGs mobilised (2025) | Over 90 lakh SHGs |

| Women covered | Over 10 crore rural women |

| States/UTs covered | All 28 states and 8 UTs |

| Core principle | Social mobilisation, financial inclusion, livelihood diversification |

Background and Historical Context

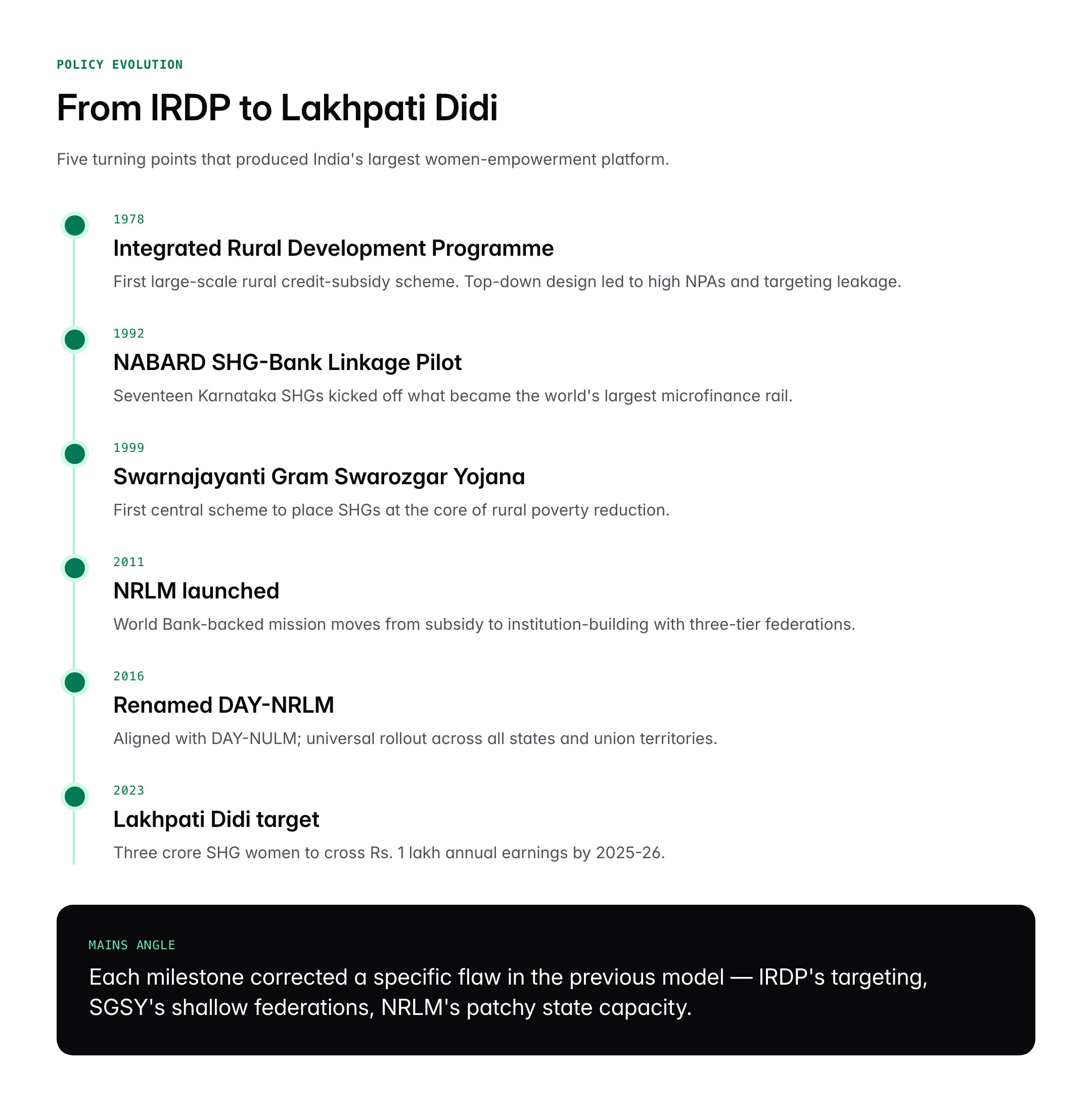

The genesis of NRLM lies in two earlier experiments. The first was the Integrated Rural Development Programme (IRDP) of 1978, which attempted income-generation through subsidised bank credit but suffered from top-down targeting, high non-performing assets and low repayment discipline. The second, more successful predecessor was the Swarnajayanti Gram Swarozgar Yojana (SGSY), launched in 1999, which introduced the Self-Help Group concept to central rural policy, drawing on the pioneering work of NABARD’s SHG-Bank Linkage Programme of 1992 and the field-tested models of Andhra Pradesh’s Velugu (later Indira Kranti Patham) and Kerala’s Kudumbashree.

By 2009 a review by the Radhakrishna Committee recommended a restructured mission that would treat poverty reduction as a time-bound campaign rather than a credit-disbursement scheme. The new design placed social mobilisation — not subsidy — at the centre. The Government of India launched NRLM in June 2011 with partial World Bank financial support through the National Rural Livelihoods Project. The mission was rolled out in a phased, intensive strategy beginning in select blocks of nine states and expanding to universal coverage by 2017.

The renaming to Deendayal Antyodaya Yojana in March 2016 reflected the government’s antyodaya (last-person-first) framing and harmonised the rural mission (DAY-NRLM) with its urban counterpart (DAY-NULM). Today NRLM is the single largest women-empowerment platform in India and one of the largest livelihood programmes in the world, with a cumulative bank credit disbursement crossing Rs. 10 lakh crore by financial year 2024-25 according to MoRD data.

Key Features

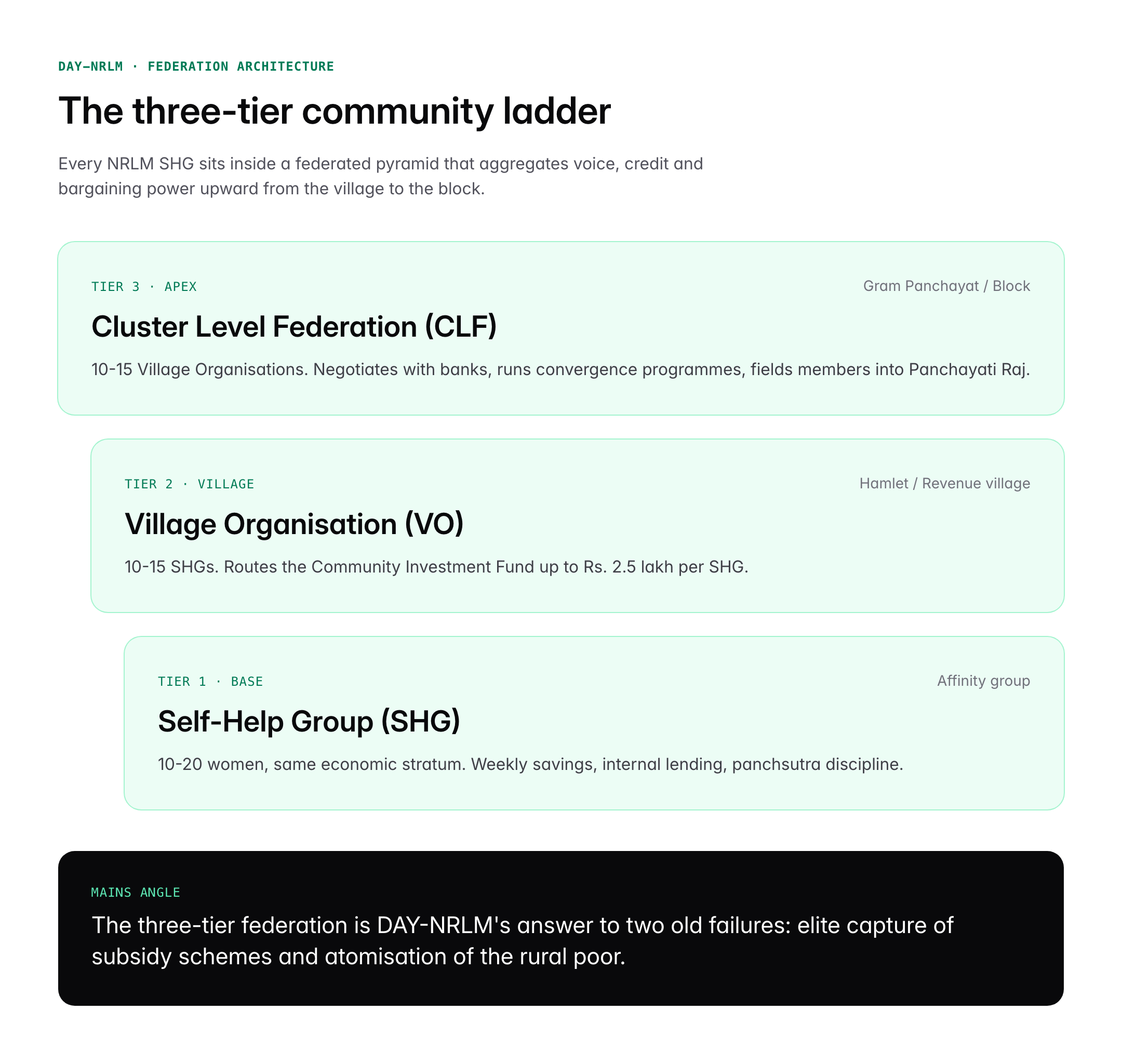

Three-Tier Community Institutional Architecture

DAY-NRLM builds a three-tier federated structure of the rural poor. At the base sits the Self-Help Group (SHG) — a voluntary affinity group of 10 to 20 women from the same economic stratum who save a fixed amount weekly and lend to each other from the common corpus. Groups of 10 to 15 SHGs at the village level federate into a Village Organisation (VO), and VOs at the Gram Panchayat or block level federate into a Cluster Level Federation (CLF). This pyramid, with CLFs at the top, gives the rural poor a collective voice, bulk bargaining power and a platform for convergence with other government schemes.

Social Mobilisation and Capacity Building

The mission deploys Community Resource Persons (CRPs) — women from mature SHGs who travel to newly mobilised blocks to train fresh members in book-keeping, panchsutra discipline and federation management. Every SHG is expected to follow the panchsutra — regular meetings, regular savings, regular internal lending, timely repayment and up-to-date books of accounts.

Financial Inclusion and Bank Linkage

NRLM provides a Revolving Fund (RF) of Rs. 20,000 to Rs. 30,000 per SHG and a Community Investment Fund (CIF) of up to Rs. 2.5 lakh per SHG routed through the VO. The most transformative lever is the SHG-Bank Linkage Programme, under which banks extend credit at 7 per cent interest with an additional 3 per cent interest subvention on prompt repayment, bringing the effective rate to just 4 per cent in 250 identified districts. The Pradhan Mantri Jan Dhan Yojana accounts and the Rupay cards issued to members complete the inclusion loop.

Livelihood Diversification — Mahila Kisan and Non-Farm Enterprises

Sub-programmes such as the Mahila Kisan Sashaktikaran Pariyojana (MKSP), Start-up Village Entrepreneurship Programme (SVEP) and the Aajeevika Grameen Express Yojana (AGEY) extend the SHG platform into sustainable agriculture, non-farm micro-enterprise and rural transport respectively.

Convergence with Other Flagship Missions

NRLM is the delivery vehicle for the Lakhpati Didi initiative (targeting 3 crore women earning over Rs. 1 lakh annually), the Drone Didi scheme, the Bank Sakhi and Pashu Sakhi cadres, and the PMAY-G Enumeration. This convergence function is unique to NRLM and distinguishes it from single-purpose credit schemes.

Significance for UPSC and General Knowledge

- NRLM is the operative example for every Mains answer on women empowerment, rural poverty reduction and cooperative federalism under GS Paper 2.

- The mission illustrates the transition from welfare-as-subsidy to welfare-as-institution-building, a key theme of the Second Administrative Reforms Commission.

- It provides concrete data for GS Paper 3 answers on financial inclusion, non-performing assets and priority-sector lending.

- The scheme is a template for South-South cooperation — delegations from Ethiopia, Bangladesh and Kenya have studied it for replication.

- It offers case material for the Ethics paper on compassion, empathy and public service motivation in community mobilisers.

- Essay topics on Gandhi’s gram swaraj, Amartya Sen’s capability approach and Bina Agarwal’s work on women and property routinely draw on SHG outcomes.

Detailed Analysis: Impact and Evidence

Peer-reviewed and official evaluations of NRLM are remarkably convergent on direction, even where they differ on magnitude. A 2020 World Bank impact evaluation of Bihar’s Jeevika project — the NRLM sister initiative — found that treatment households saw a 22 per cent reduction in high-cost informal debt, a 27 per cent rise in women’s workforce participation and a statistically significant decline in the share of women reporting domestic violence. The study is now the standard reference for rural mobilisation economics in South Asia.

A NITI Aayog assessment published in 2023 reported that SHG members in DAY-NRLM blocks had 19 per cent higher monthly household income than non-members in comparable geographies, with the largest gains accruing to Scheduled Caste and Scheduled Tribe households. The repayment rate across the SHG-Bank Linkage Programme has held above 96 per cent, a figure unmatched by any comparable unsecured-credit programme in the commercial banking sector, according to NABARD’s Status of Microfinance in India reports.

On the non-economic side, studies by the Institute of Rural Management Anand (IRMA) and the Indian Institute of Management Ahmedabad have documented a measurable rise in women’s mobility, participation in Gram Sabha meetings and aspirations for girl children’s education in NRLM villages. The Kudumbashree network in Kerala, the most mature SHG federation, today operates its own micro-enterprises, runs neighbourhood old-age care services and has fielded thousands of women candidates in Panchayati Raj elections.

However, the mission’s geography remains uneven. Bihar, Andhra Pradesh, Telangana, Odisha and West Bengal account for a disproportionate share of mature SHGs and credit volumes, while Uttar Pradesh, Madhya Pradesh and Rajasthan — despite housing a large share of poor households — show slower institutional maturity. Closing this gap is the central challenge for the 2025-30 phase of the mission.

Comparative Perspective

| Feature | DAY-NRLM (India) | Grameen Bank (Bangladesh) | BRAC Ultra-Poor (Bangladesh) | Kudumbashree (Kerala, subsumed under NRLM) |

|---|---|---|---|---|

| Primary unit | SHG of 10-20 women | Group of 5 borrowers | Individual ultra-poor women | Neighbourhood Group (NHG) of 10-20 women |

| Core instrument | Savings + bank-linked credit | Joint-liability micro-loan | Asset transfer + stipend + training | Savings + thrift + micro-enterprise |

| Federation | Three-tier (SHG/VO/CLF) | Centre-based, no federation | Graduation cohorts | Three-tier (NHG/ADS/CDS) |

| Interest to borrower | 4-7 per cent after subvention | 20 per cent declining | Grant component + soft loan | 4-9 per cent |

| Public funding | Centre-state 60:40 | Member-owned bank | Donor-funded NGO | Kerala state + NRLM |

The comparison underlines NRLM’s distinctive feature — it is a government-led mobilisation at continental scale, whereas Grameen and BRAC are private-sector or NGO models with deeper per-household intensity but narrower reach.

Challenges and Criticisms

Despite its achievements, NRLM faces structural challenges. First, the mission’s reliance on state-level implementation capacity produces wide disparities; a State Rural Livelihood Mission (SRLM) in Bihar or Andhra Pradesh is institutionally light-years ahead of one in a laggard state. Second, the absence of a portability mechanism for SHG membership means that migrant women lose access to credit when they move to cities for work. Third, the average loan ticket size remains small relative to the capital required for transformative micro-enterprise, and graduation from consumption smoothing to productive investment is slow.

Critics also point to over-indebtedness risks as commercial micro-finance institutions piggy-back on NRLM-mobilised SHGs, sometimes offering multiple loans to the same household and driving distress. The CAG has flagged instances of inactive or defunct SHGs continuing to appear on the online list, inflating outreach numbers. Finally, patriarchal household dynamics mean that loans taken in women’s names are frequently controlled by male members — a qualitative finding that no dashboard captures.

Prelims Pointers

- DAY-NRLM is administered by the Ministry of Rural Development under the Deendayal Antyodaya Yojana umbrella.

- NRLM was launched in June 2011 and renamed DAY-NRLM on 29 March 2016.

- Funding pattern is 60:40 between Centre and states, and 90:10 for North-East and Himalayan states.

- The SHG-Bank Linkage Programme was originally piloted by NABARD in 1992.

- Interest subvention lowers the effective rate to 4 per cent in 250 identified districts.

- MKSP targets women farmers; SVEP targets non-farm enterprises; AGEY targets rural transport.

- Kudumbashree (Kerala) and Jeevika (Bihar) are the best-known state rural livelihood missions.

- The three-tier structure is SHG, Village Organisation (VO) and Cluster Level Federation (CLF).

- The World Bank supported the rollout through the National Rural Livelihoods Project (NRLP).

- The Lakhpati Didi scheme aims to make 3 crore SHG women earn more than Rs. 1 lakh per year.

- Over 90 lakh SHGs and 10 crore women have been mobilised under DAY-NRLM by 2025.

- Repayment rates in SHG-Bank linkage exceed 96 per cent, much higher than commercial unsecured credit.

Mains Practice Questions

- “The Deendayal Antyodaya Yojana National Rural Livelihoods Mission has shifted rural poverty reduction from subsidy-delivery to institution-building.” Critically examine.

- Contrast IRDP and SGSY design failures with NRLM’s social-mobilisation-first architecture.

- Cite Jeevika and Kudumbashree outcomes on income, mobility and political participation.

- Discuss pending gaps — portability, graduation, uneven state capacity — and reforms needed.

- Discuss the role of Self-Help Groups in promoting financial inclusion and gender empowerment in rural India, with reference to the DAY-NRLM.

- Outline the three-tier architecture and the SHG-Bank Linkage Programme.

- Present evidence on women’s workforce participation, credit access and domestic outcomes.

- Conclude on convergence with PMJDY, PMAY-G and the Lakhpati Didi initiative.

Conclusion

The NRLM SHG list is not just an administrative database; it is the membership roll of the largest organised community of poor women on earth. Over fourteen years, DAY-NRLM has redefined the Indian state’s relationship with rural households — from delivering benefits to enabling collectives, from issuing cheques to issuing voice. Its institutional rails now carry a wide spectrum of convergence programmes, from affordable housing and LPG connections to digital payments and climate-resilient agriculture.

The next chapter of the mission must address the qualitative deficits that quantitative dashboards cannot see — membership portability for migrant women, sharper livelihoods graduation, the quality of democratic practice inside federations, and the replacement of inactive SHGs in the public list. If these are solved, NRLM will complete India’s most important social experiment of the twenty-first century — converting the poorest women of the republic into credit-worthy, enterprise-running, politically active citizens of a gram swaraj their grandchildren will inherit.

Frequently Asked Questions

What is the NRLM SHG list?

The NRLM SHG list is the publicly accessible database of Self-Help Groups registered under the Deendayal Antyodaya Yojana National Rural Livelihoods Mission, hosted on the Ministry of Rural Development portal. It contains details of over 90 lakh SHGs and more than 10 crore rural women members across every state and union territory in India.

Why is DAY-NRLM important for UPSC preparation?

DAY-NRLM is a core reference for UPSC GS Paper 2 questions on welfare schemes, women empowerment and cooperative federalism. It also provides case material for GS Paper 3 on financial inclusion, for the Essay paper on gram swaraj and for the Ethics paper on public service motivation among community resource persons.

How is NRLM related to the SHG-Bank Linkage Programme?

The SHG-Bank Linkage Programme, pioneered by NABARD in 1992, is the financial rail on which NRLM runs. Mature NRLM SHGs become eligible for direct bank credit at 7 per cent interest, further reduced to an effective 4 per cent in 250 identified districts through the prompt-repayment interest subvention.

When was NRLM renamed Deendayal Antyodaya Yojana?

NRLM was launched in June 2011 as the restructured successor to the Swarnajayanti Gram Swarozgar Yojana. It was renamed the Deendayal Antyodaya Yojana National Rural Livelihoods Mission on 29 March 2016 to align with the government’s antyodaya framing and with the urban DAY-NULM scheme.

What is the three-tier SHG federation structure under NRLM?

At the base are Self-Help Groups of 10-20 women. Ten to fifteen SHGs federate at village level into a Village Organisation, and VOs federate at the Gram Panchayat or block level into a Cluster Level Federation. This architecture gives poor women bargaining power, institutional voice and convergence access.

How much credit has flowed to SHGs under NRLM?

By financial year 2024-25 the cumulative bank credit disbursed to NRLM SHGs under the SHG-Bank Linkage Programme had crossed Rs. 10 lakh crore according to Ministry of Rural Development data. The repayment rate consistently exceeds 96 per cent, far higher than commercial unsecured lending.

What is the Lakhpati Didi scheme?

The Lakhpati Didi initiative, announced in 2023 and expanded in 2024, targets converting three crore NRLM SHG women into annual earners of over Rs. 1 lakh through sustainable livelihoods, skilling, credit access and convergence with schemes like Drone Didi, Bank Sakhi and the Start-up Village Entrepreneurship Programme.

What are the main challenges facing DAY-NRLM?

Key challenges include uneven implementation capacity across states, the absence of membership portability for migrant women, slow graduation from consumption credit to productive enterprise, risks of over-indebtedness from parallel microfinance lending, and the continued listing of defunct SHGs that inflate official outreach numbers.