Introduction

The Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund, better known by its acronym PM CARES, was set up on 27 March 2020 as a public charitable trust during the first wave of the Covid-19 pandemic. It was created to receive voluntary donations for pandemic relief, healthcare infrastructure, oxygen plants, ventilators and ancillary expenditure that the government argued could not wait for regular budgetary channels. Within weeks, contributions crossed several thousand crore, making PM CARES one of the largest disaster-relief instruments ever assembled in India.

Six years on, PM CARES is a recurring flashpoint in Indian public administration. Its legal character as a trust rather than a government fund, its exclusion from the Comptroller and Auditor General’s audit, and its contested status under the Right to Information Act have pushed it into the Supreme Court and the Delhi High Court on multiple occasions. For UPSC aspirants, the Fund is a worked example of accountability, transparency, emergency finance and the tension between executive agility and public scrutiny. This guide explains its origin, governance, receipts, controversies and reform pathways.

Quick Facts at a Glance

| Attribute | Detail |

|---|---|

| Full name | Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund |

| Commonly called | PM CARES Fund |

| Constituted on | 27 March 2020 |

| Legal nature | Public charitable trust registered under the Registration Act, 1908 |

| Registered in | New Delhi |

| Ex-officio Chairperson | Prime Minister of India |

| Ex-officio Trustees | Minister of Home Affairs, Minister of Finance, Minister of Defence |

| Nominated trustees | Three eminent persons nominated by the Chairperson |

| Income-tax status | Section 80G (100 per cent deduction) |

| CSR status | Eligible under Schedule VII of Companies Act, 2013 |

| FCRA clearance | Exempted under Section 50 of FCRA, 2010 |

| Audit | By independent auditor, not CAG |

| Key stated object | Emergency or distress relief, including Covid-19 |

Background and Historical Context

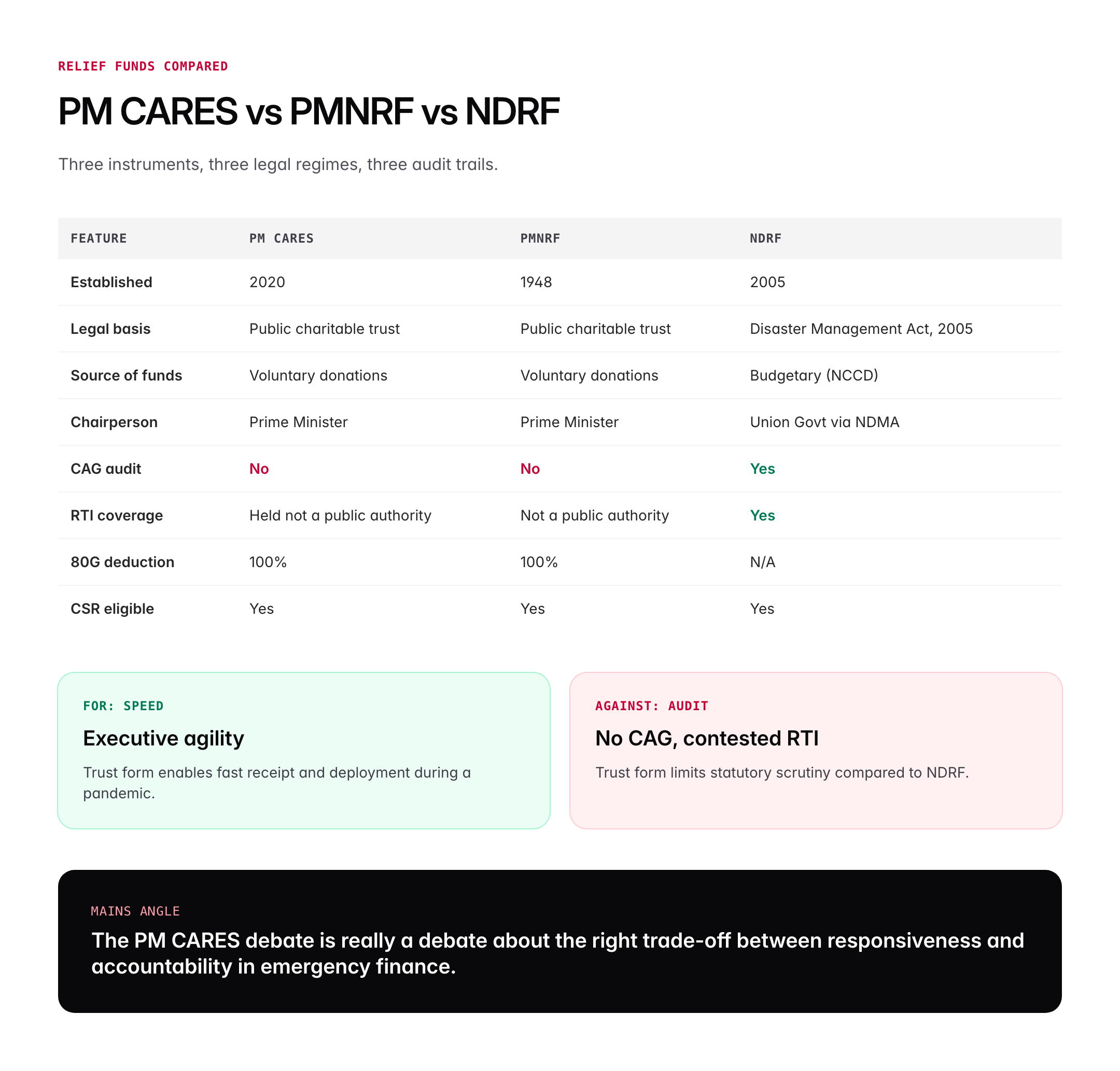

India has long operated a dedicated disaster-relief vehicle in the form of the Prime Minister’s National Relief Fund, or PMNRF, set up in January 1948 by Jawaharlal Nehru to assist displaced persons from Pakistan. Over time PMNRF evolved into a general-purpose relief fund for natural calamities, accidents, riot victims and medical treatment. It is unaudited by the CAG, is not backed by any statute, and sits outside the Consolidated Fund of India. PMNRF’s design became the template for later relief mechanisms.

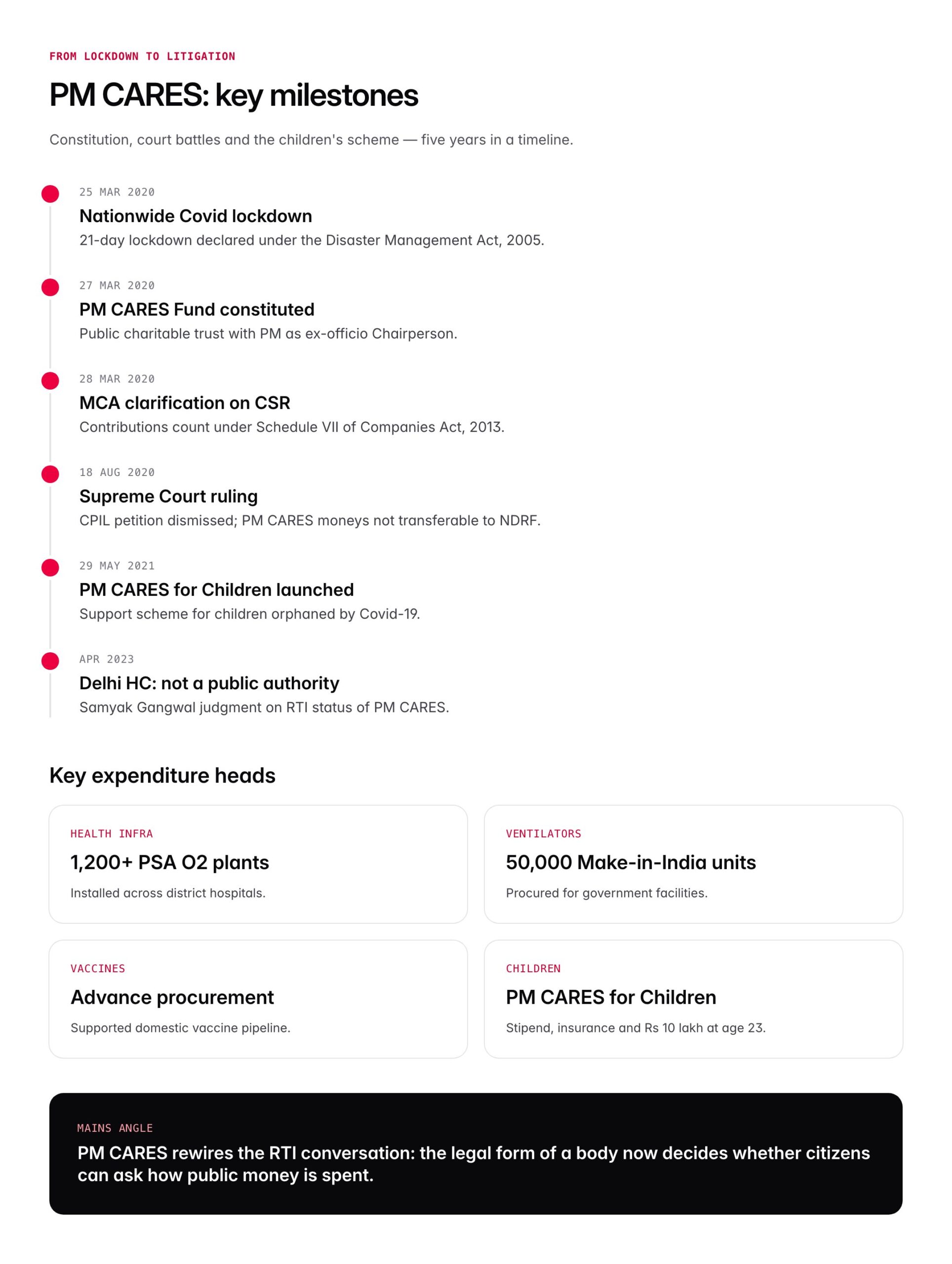

When Covid-19 reached India in early 2020 and the nationwide lockdown was imposed on 25 March 2020, the government argued that the existing PMNRF was insufficient in scale and ambition. On 27 March 2020, the PM CARES Fund was created as a separate public charitable trust. The declared justifications were three-fold: speed of response, ability to accept corporate CSR contributions, and signalling a specific emergency vehicle for pandemic relief. The Fund was publicised within days and received a large volume of individual, corporate and foreign donations.

The legal architecture is modelled loosely on the PMNRF, with some important differences. Both are public charitable trusts and both have the Prime Minister as Chairperson. Unlike PMNRF, PM CARES includes the Ministers of Home, Finance and Defence as ex-officio trustees. Unlike PMNRF, PM CARES has an express provision allowing CSR contributions to count towards the company’s Schedule VII obligations under the Companies Act, 2013. Unlike PMNRF, PM CARES accepts foreign contributions, which under ordinary FCRA rules would require registration; a special Section 50 exemption was issued.

Key Features of the Trust

Governance and trustees

The Prime Minister serves as ex-officio Chairperson. The Minister of Home Affairs, the Minister of Finance and the Minister of Defence serve as ex-officio Trustees. The Chairperson may nominate three eminent persons in the fields of research, health, science, social work, law, public administration or philanthropy as additional trustees. The trust functions through a secretariat housed in the Prime Minister’s Office.

Objects of the Fund

The declared objects include undertaking and supporting relief or assistance of any kind relating to a public health emergency, disaster or calamity, rendering financial assistance or support to the affected population, creating or upgrading healthcare or pharmaceutical facilities, and undertaking any other activity not inconsistent with the above. These objects are broad, giving the trust wide latitude in expenditure.

Revenue and receipts

The Fund receives voluntary donations from individuals, Indian companies, foreign nationals, foreign organisations, public sector enterprises, government employees through salary deductions, and interest on deposits. According to the audited financial statements placed on the Fund’s website, receipts in 2019-20 stood at around Rs 3,076 crore; in 2020-21 at around Rs 10,990 crore; and in 2021-22 at around Rs 10,990 crore, with steadily declining levels thereafter as the acute Covid phase ended. Voluntary contributions have constituted the bulk.

Expenditure priorities

Published allocations have covered procurement of ventilators, installation of Pressure Swing Adsorption oxygen plants in government hospitals, supply of vaccines, migrant welfare, support to the PM CARES for Children scheme announced in May 2021 for children who lost both parents to Covid, and research and development grants. Specific allocations include 50,000 Make-in-India ventilators, over 1,200 PSA oxygen plants across districts, and a corpus for the children’s scheme that provides a monthly stipend from age 18 and a lumpsum at age 23.

Tax and CSR status

Donations to PM CARES qualify for 100 per cent deduction under Section 80G of the Income-tax Act, 1961, equivalent to PMNRF. Corporate contributions qualify as CSR expenditure under Schedule VII of the Companies Act, 2013, following a Ministry of Corporate Affairs clarification dated 28 March 2020. This tax and CSR alignment is central to the Fund’s fundraising velocity.

Significance for UPSC and General Knowledge

- PM CARES is a live case study of GS2 themes on accountability, transparency and the RTI regime.

- It illustrates the legal distinction between a public charitable trust and a government body, a distinction central to Article 12 of the Constitution and the definition of State.

- The Fund’s CAG-audit exclusion and the parallel CAG audit of PMNRF inform debates on financial accountability of extra-budgetary instruments.

- PM CARES appears in GS3 discussions on disaster management, epidemic preparedness and corporate social responsibility.

- The PM CARES for Children scheme feeds into GS1 and GS2 themes on child welfare, orphan care and social security.

- The Supreme Court judgment of 18 August 2020 in Centre for Public Interest Litigation v. Union of India is a compact illustration of judicial deference in matters of emergency finance.

Detailed Analysis: Accountability Architecture

The debate over PM CARES turns on a deceptively simple question: is it a public authority under the Right to Information Act, 2005, and therefore subject to proactive disclosure, or is it a private charitable trust, and therefore subject only to trust law and ordinary income-tax reporting? The government has consistently argued the latter. In replies to RTI applications filed since mid-2020, the PMO and the Fund’s secretariat have held that PM CARES is not a public authority within the meaning of Section 2(h) of the RTI Act because it was not constituted by or under any statute, notification or direct executive order in the classical sense.

Petitioners have advanced several counter-arguments. The trust uses the Prime Minister’s name, national emblem and the gov.in domain. Its Chairperson is the Prime Minister in his ex-officio capacity, and three of its four standing trustees are Union Cabinet Ministers. It is housed in the Prime Minister’s Office. Government employees can contribute through salary deductions. It enjoys unique FCRA, CSR and Section 80G advantages that no ordinary private trust receives. These indicia, they argue, bring the Fund within the expanded definition of public authority under the RTI Act. The Delhi High Court in Samyak Gangwal v. PIO, PM CARES Fund (2023) held that the Fund is not a public authority under the RTI Act but directed limited disclosure of certain documents.

The CAG audit question has a similar texture. Under Article 149 of the Constitution and the CAG’s Duties, Powers and Conditions of Service Act, 1971, the CAG audits accounts of the Union and states, all bodies substantially financed by government revenues, and government companies. PM CARES, composed of voluntary donations and not of budgetary outlays, falls outside this perimeter. Its accounts are audited annually by an independent chartered accountant firm, currently SARC Associates, and the audited statements are placed on the Fund’s website. Critics argue that a body chaired by the Prime Minister and housed in his office ought to meet a higher standard of public audit than an ordinary trust.

The Supreme Court, in its 18 August 2020 order in Centre for Public Interest Litigation, declined to transfer PM CARES moneys to the National Disaster Response Fund. The court held that NDRF and PM CARES serve different legal regimes, that voluntary donors cannot be compelled to redirect their contributions, and that the separate existence of PM CARES does not violate the Disaster Management Act, 2005. The judgment is short and is often criticised as deferential, but it is the leading authority on the question.

Comparative Perspective

Placing PM CARES alongside other relief and emergency instruments clarifies what is new and what is not.

| Feature | PM CARES | PMNRF | NDRF | CM Relief Funds |

|---|---|---|---|---|

| Year established | 2020 | 1948 | 2005 | Various |

| Legal basis | Public charitable trust | Public charitable trust | Disaster Management Act, 2005 | State-level trusts |

| Source | Voluntary donations | Voluntary donations | Budgetary allocation via NCCD | Voluntary donations + state top-up |

| CAG audit | No | No | Yes | Generally no |

| RTI coverage | Contested; court held not public authority | Not public authority | Yes | Varies |

| CSR eligible | Yes | Yes | Yes | Yes (state-specific) |

| Chairperson | PM | PM | NDMA Vice-Chair indirectly | CM |

The structural similarity between PM CARES and PMNRF is striking. Both are public charitable trusts. Both are chaired by the Prime Minister. Both are outside the CAG audit and, as per the current judicial reading, outside the RTI definition of public authority. What PM CARES has done is not invent a new accountability regime but transplant an existing one onto a new and much larger instrument, with CSR and FCRA add-ons that PMNRF never had.

Controversies and Debates

Three debates surround PM CARES. First is the transparency debate. Critics argue that any fund chaired by the Prime Minister, using the national emblem and the gov.in domain, should meet the full disclosure standards of a government body. Supporters respond that transparency is met through annual audited financial statements, a public website and ministry CSR disclosures, and that applying the RTI Act would chill voluntary donations.

Second is the federalism debate. Several opposition-ruled states argued in 2020 that PM CARES bypassed the existing NDRF and State Disaster Response Funds envisaged under the Disaster Management Act, 2005, concentrating emergency finance at the Centre. The Supreme Court rejected the challenge in August 2020 but the underlying concern about fiscal federalism remains a live GS2 topic. Supporters argue that the NDRF and PM CARES are complementary, one statutory and budgetary, the other voluntary and supplementary.

Third is the CSR debate. When the Ministry of Corporate Affairs clarified that contributions to PM CARES count as CSR under Schedule VII, but similar clarifications were slower for CM Relief Funds, several states complained of unequal treatment. A subsequent circular treated CM Relief Funds on a par in some respects, but the original asymmetry fed perceptions that PM CARES was structurally privileged. The MCA has since notified balanced rules, but the GS2 analytical point about neutrality of CSR incentives remains.

Prelims Pointers

- PM CARES was constituted on 27 March 2020.

- It is a public charitable trust registered under the Registration Act, 1908.

- The Prime Minister is ex-officio Chairperson.

- Ministers of Home, Finance and Defence are ex-officio Trustees.

- Three nominated trustees may be added by the Chairperson.

- Donations to PM CARES qualify for 100 per cent deduction under Section 80G of the Income-tax Act, 1961.

- Contributions count as CSR under Schedule VII of the Companies Act, 2013.

- PM CARES has a special exemption under Section 50 of FCRA, 2010 to accept foreign contributions.

- Its accounts are audited by an independent auditor, not by the CAG.

- The Delhi High Court in 2023 held that PM CARES is not a public authority under the RTI Act.

- The Supreme Court in August 2020 declined to transfer PM CARES moneys to NDRF.

- PM CARES for Children scheme was announced on 29 May 2021.

Mains Practice Questions

- Critically examine the accountability framework governing the PM CARES Fund against the standards set for statutory emergency instruments under the Disaster Management Act, 2005.

- Describe PM CARES as a public charitable trust and NDRF as a statutory fund.

- Compare audit, RTI, parliamentary oversight and donor transparency across the two.

- Argue for reform pathways including voluntary CAG audit and proactive disclosure under RTI principles.

- The PM CARES Fund raises fundamental questions about the reach of the Right to Information Act, 2005 and the constitutional conception of public authority. Discuss with reference to relevant case law.

- Explain Section 2(h) of the RTI Act and the expansive tests in Thalappalam Service Cooperative Bank and Aditya Bandopadhyay.

- Narrate the Samyak Gangwal ruling and its reasoning.

- Evaluate whether the outcome satisfies the constitutional purpose of transparency.

Conclusion

PM CARES is a study in the tension between executive agility and public accountability. Born in the emergency of the Covid-19 lockdown, it demonstrated that India’s federal state can mobilise voluntary capital at speed, channel it into frontline healthcare infrastructure and a children’s welfare scheme, and sustain donor confidence through annual audited statements. In that sense it has earned its place alongside PMNRF as a recognised national relief instrument.

At the same time, PM CARES illustrates how the governance of emergency finance in India remains lightly regulated. The same trust structure that permits speed also limits statutory audit and RTI reach. As the country builds its disaster preparedness architecture for the next decade, PM CARES offers the most concrete live case for asking how voluntary and statutory relief mechanisms should be organised, audited and made accountable without compromising the responsiveness that made the Fund possible in the first place. That is where the GS2 conversation will continue.

Frequently Asked Questions

What is the PM CARES Fund?

The PM CARES Fund, full name Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund, is a public charitable trust created on 27 March 2020 to receive voluntary donations for Covid-19 relief and other public health emergencies. It is chaired by the Prime Minister, registered under the Registration Act, 1908, and supports health infrastructure, oxygen plants, vaccines and the PM CARES for Children scheme.

Why is PM CARES important for UPSC?

PM CARES is a live GS2 case study on accountability, transparency, RTI coverage and emergency finance. It connects to GS3 disaster management through its interaction with the Disaster Management Act, 2005 and the National Disaster Response Fund. Questions on its legal status, CAG audit exclusion and Supreme Court rulings appear frequently in Prelims and Mains.

How is PM CARES different from PMNRF?

Both are public charitable trusts chaired by the Prime Minister. PM CARES adds the Home, Finance and Defence Ministers as ex-officio trustees, has explicit CSR eligibility under Schedule VII of the Companies Act, 2013, and enjoys a special FCRA Section 50 exemption for foreign donations. PMNRF, set up in 1948, predates the CSR and FCRA regimes and has a narrower tax-legal footprint.

Is PM CARES covered under the Right to Information Act?

Not directly. The Delhi High Court in Samyak Gangwal v. PIO, PM CARES Fund (2023) held that the Fund is not a public authority under Section 2(h) of the RTI Act, 2005, because it is a public charitable trust rather than a body constituted by or under any statute or government notification. Limited disclosure of specific documents has been directed in some cases.

Is PM CARES audited by the CAG?

No. Under Article 149 of the Constitution and the CAG Act of 1971, the Comptroller and Auditor General audits only bodies substantially financed by government revenues. PM CARES is composed entirely of voluntary donations and is not financed from the Consolidated Fund of India. Its accounts are audited annually by an independent chartered accountant firm and placed on the Fund’s website.

Do donations to PM CARES qualify as CSR?

Yes. A Ministry of Corporate Affairs clarification dated 28 March 2020 specified that contributions by companies to PM CARES count as Corporate Social Responsibility expenditure under Schedule VII of the Companies Act, 2013. Donations also qualify for 100 per cent deduction under Section 80G of the Income-tax Act, 1961 in the hands of individual and corporate donors.

What is the PM CARES for Children scheme?

Announced on 29 May 2021, PM CARES for Children supports children who lost both parents, surviving parent, legal guardian or adoptive parents to Covid-19. Beneficiaries receive scholarship support, free education, health insurance, a monthly stipend from age 18 and a lumpsum of Rs 10 lakh at age 23. The scheme is financed entirely from the PM CARES Fund.

How did the Supreme Court rule on PM CARES?

In Centre for Public Interest Litigation v. Union of India, decided on 18 August 2020, the Supreme Court declined to transfer PM CARES moneys to the National Disaster Response Fund. The court held that NDRF and PM CARES operate under different legal regimes, that donors cannot be compelled to redirect voluntary contributions, and that PM CARES does not contravene the Disaster Management Act, 2005.