Introduction

The shift from cheques to real-time payments has reshaped how money moves through the Indian economy. At the centre of this transformation sit two Reserve Bank of India (RBI) payment rails, NEFT and RTGS. The question about neft meaning is a routine search query for account holders, but for a UPSC aspirant it opens a much richer window into the payments architecture, financial inclusion and the regulatory stewardship of the RBI.

This article unpacks the NEFT full form, explains how it differs from RTGS, surveys timings, charges and transaction limits, and places both systems in the broader context of India’s digital payments revolution. Readers will leave with a clear grasp of which rail to use for a given transfer and with enough policy context to answer GS3 Economy questions on financial infrastructure.

Quick Facts at a Glance

| Item | NEFT | RTGS |

|---|---|---|

| Full form | National Electronic Funds Transfer | Real Time Gross Settlement |

| Launched | November 2005 | March 2004 |

| Operator | Reserve Bank of India | Reserve Bank of India |

| Settlement type | Deferred, in half-hourly batches | Real-time, gross, transaction by transaction |

| Minimum amount | No minimum | Rs 2 lakh |

| Maximum amount | No upper cap (bank may set) | No upper cap |

| Availability | 24x7x365 (since 16 December 2019) | 24x7x365 (since 14 December 2020) |

| Online charges | Nil for savings account customers (since January 2020) | Nil for online initiation (as per RBI) |

| Offline service charge | Capped by RBI | Capped by RBI |

| Cheque equivalent | No | No |

Background and Historical Context

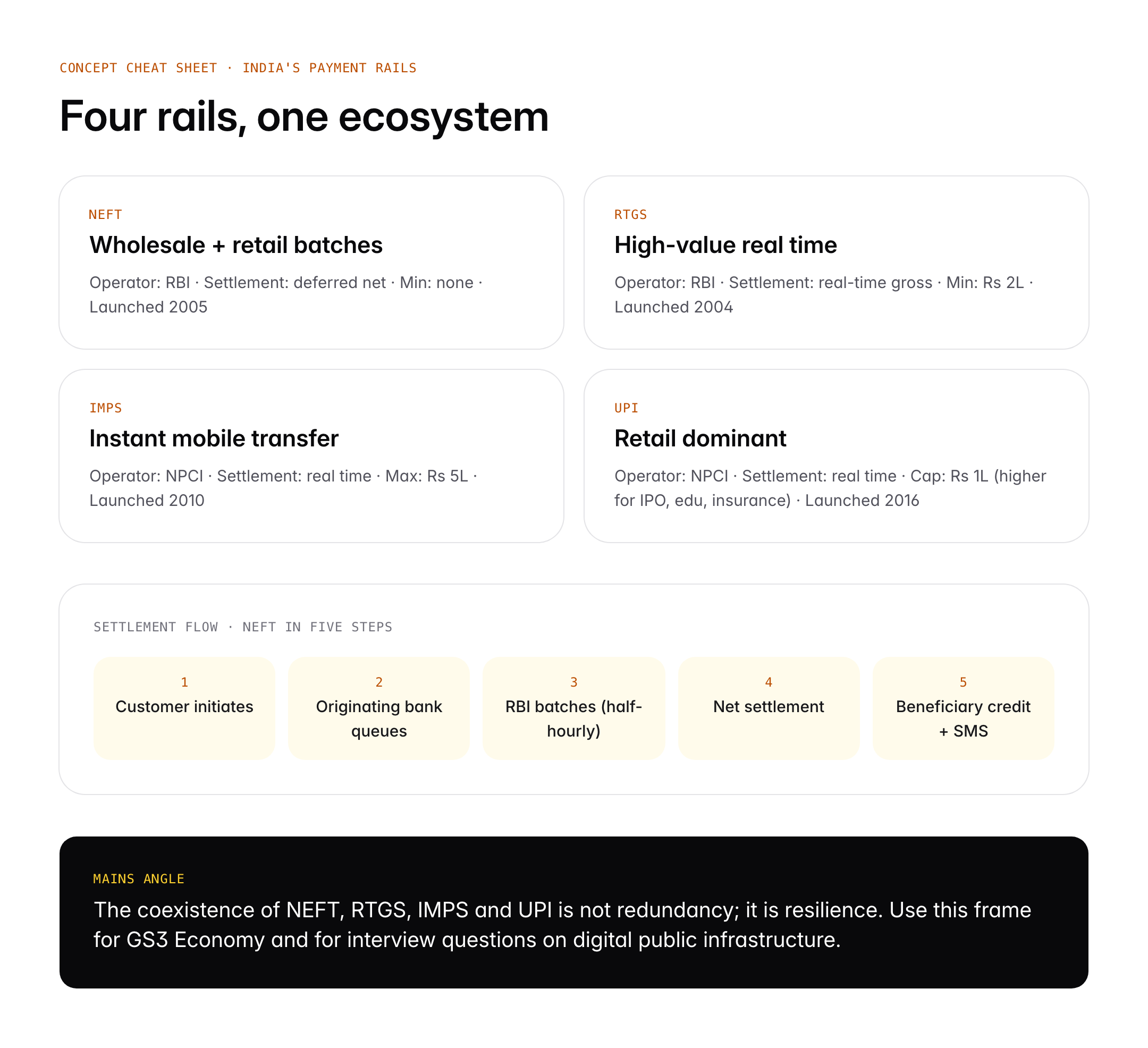

India’s modern electronic payments era began when the RBI replaced the older Special Electronic Funds Transfer (SEFT) system with NEFT in November 2005. SEFT itself had succeeded the Electronic Funds Transfer scheme of the late 1990s. NEFT introduced a nationwide, bank-neutral mechanism that worked in deferred batches, allowing any customer of a participating bank to send money to any other participating bank.

RTGS, launched in March 2004, predated NEFT and served a different need. It was designed for high-value, time-critical payments where credit had to be instantaneous and irrevocable. Banks, corporates and government treasuries became the early users. Because RTGS settles each transaction individually on a gross basis against the bank’s RBI current account, it is the backbone of wholesale payments in the country.

The payments system expanded rapidly through the 2010s with the creation of the National Payments Corporation of India (NPCI) in 2008 as an umbrella organisation, the launch of the Immediate Payment Service (IMPS) in 2010 and the Unified Payments Interface (UPI) in 2016. Even so, NEFT and RTGS remain the backbone of bank-to-bank transfers because they are owned and operated directly by the RBI under the Payment and Settlement Systems Act, 2007.

Two 2020 reforms cemented their modern status. The RBI made NEFT available 24x7x365 on 16 December 2019 and extended the same round-the-clock access to RTGS on 14 December 2020, making India one of the first major economies to offer continuous real-time large-value settlement.

Key Features

What NEFT means

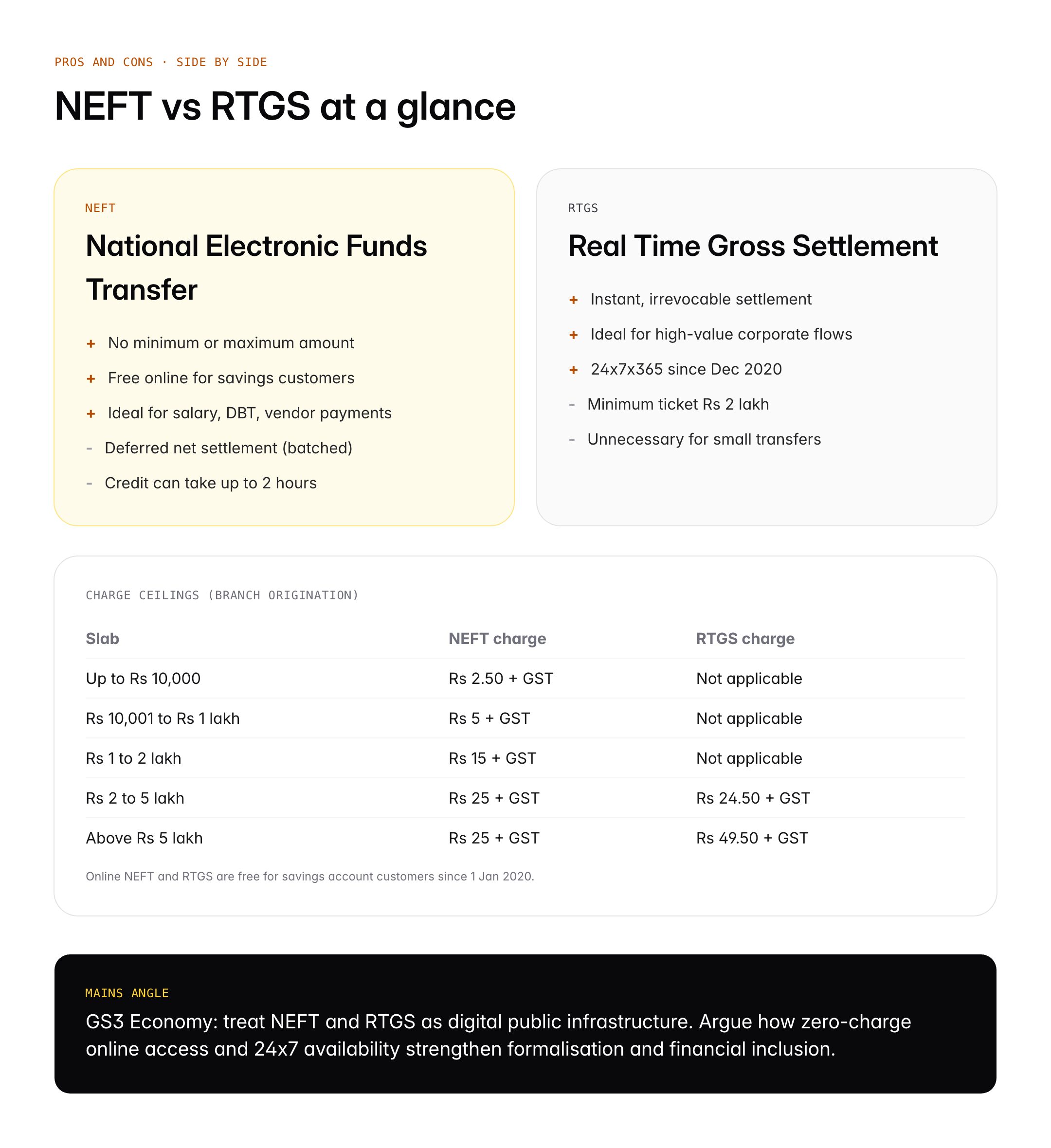

NEFT, the National Electronic Funds Transfer, is a nationwide centralised payment system owned and operated by the Reserve Bank of India. A customer initiates a transfer online or through a branch. The originating bank sends the message to the RBI’s NEFT clearing centre, which batches instructions and settles them at half-hourly intervals. Once the beneficiary bank credits the account, the originator receives confirmation. NEFT works on a deferred net settlement (DNS) basis, which means the RBI computes net obligations across banks before moving money.

What RTGS means

RTGS, Real Time Gross Settlement, settles each transaction individually, in real time, on a gross basis, irrevocably. There is no batching or netting. The moment the RBI settles a leg, it is final. RTGS is mandatory for customer transactions of Rs 2 lakh and above; below that threshold it is not available.

Transaction limits

NEFT has no minimum or maximum limit prescribed by the RBI. Individual banks may cap per-transaction or daily amounts, especially for internet banking channels not using two-factor authentication. Branch-initiated NEFTs typically have higher limits subject to KYC. RTGS has a regulatory minimum of Rs 2 lakh and no upper cap; banks may fix prudential limits for retail users.

Timings

Both NEFT and RTGS are 24x7x365. NEFT settles in 48 half-hourly batches each day, starting at 00:30 and ending at 00:00 of the next day. RTGS is continuous; every instruction is settled as soon as it is received, subject to liquidity in the remitter bank’s RBI account.

Charges

The RBI abolished processing charges on online NEFT and RTGS for savings bank customers from 1 January 2020, as part of the push for digital payments. Banks may still levy small fees on branch-originated transfers, subject to an RBI ceiling: up to Rs 2.50 plus GST for NEFT amounts up to Rs 10,000 and up to Rs 25 plus GST for amounts above Rs 2 lakh; RTGS charges at the branch are capped at Rs 24.50 plus GST for Rs 2 lakh to Rs 5 lakh and Rs 49.50 plus GST above Rs 5 lakh.

Legal framework

Both systems operate under the Payment and Settlement Systems Act, 2007, which empowers the RBI to regulate and supervise payment systems. The RBI also frames the Positive Pay System for cheques, the Digital Payments Index (DPI) for tracking adoption, and the Vision Document on Payment Systems that updates goals every three years.

Significance for UPSC and General Knowledge

- Directly tested in Prelims current affairs on payments, RBI functions and financial inclusion

- Supports Mains GS3 answers on banking reform, digital economy and formalisation

- Links to essay topics on technology and governance, and financial sector resilience

- Relevant to Economy optional and to RBI Grade B examinations

- Useful for interview questions on everyday banking and fintech policy

- Helps distinguish payment systems (NEFT, RTGS, IMPS, UPI, AePS, NACH) for factual precision

Detailed Analysis: Payment Systems and the Digital Economy

India’s payment systems form a layered architecture. At the wholesale level, RTGS handles inter-bank settlements, government securities transactions through the Negotiated Dealing System, and high-value corporate flows. At the retail level, NEFT, IMPS, UPI, NACH and AePS serve different niches. IMPS, run by NPCI, caters to interbank mobile-initiated payments with 24×7 availability since 2010 and a limit of Rs 5 lakh. UPI, layered on top of IMPS, has become the dominant retail rail with a per-transaction limit of Rs 1 lakh for most categories and higher limits for education, healthcare, initial public offerings and insurance.

The digital payments surge since demonetisation in November 2016 has been striking. According to the RBI Digital Payments Index, the aggregate value of digital payments in India crossed 15 times between March 2014 and March 2024. NEFT continues to record over 700 million transactions and more than Rs 400 lakh crore in value every year. UPI leads volume, but NEFT and RTGS dominate on value terms because of their role in large settlements.

The Unified Payments Interface does not replace NEFT and RTGS; it rides on a different backbone. Corporates, exporters, government departments and treasuries still prefer RTGS for irrevocable, high-value flows, while NEFT remains the default for standing instructions, salary disbursements and cross-bank transfers that exceed the UPI cap.

The RBI’s 2020 decision to make both NEFT and RTGS membership open to non-bank Payment System Operators, including prepaid payment instrument issuers, card networks and White-Label ATM operators, has deepened the ecosystem. Since 2021 these entities can directly participate in central bank payment rails, reducing dependence on sponsor banks. The CBDC (Central Bank Digital Currency) pilot for e-Rupee, launched in 2022, adds another layer to the payments stack.

Financial inclusion through the Jan Dhan-Aadhaar-Mobile (JAM) trinity, the Pradhan Mantri Jan Dhan Yojana (PMJDY) and the Direct Benefit Transfer (DBT) system has expanded the user base of NEFT-linked accounts. By 2024, over 53 crore Jan Dhan accounts had been opened, many of which receive DBT through NEFT-style bulk credit.

Comparative Perspective

| Feature | NEFT | RTGS | IMPS | UPI |

|---|---|---|---|---|

| Operator | RBI | RBI | NPCI | NPCI |

| Settlement | Deferred net | Real time gross | Real time | Real time |

| Min amount | None | Rs 2 lakh | Re 1 | Re 1 |

| Max amount | Bank-set | None (banks set) | Rs 5 lakh | Rs 1 lakh (higher for specified categories) |

| Availability | 24x7x365 | 24x7x365 | 24x7x365 | 24x7x365 |

| Channel | Branch, net banking | Branch, net banking | Mobile, net banking | Mobile apps |

| Typical use | Salary, vendor payments | Corporate, treasury | Peer to peer | Retail, peer to peer |

Globally, RTGS-style systems include FEDWIRE in the United States, TARGET2 in the Eurozone and CHAPS in the United Kingdom. Retail equivalents of NEFT and UPI include the US FedNow, the UK Faster Payments and Brazil’s PIX. India’s combination of free retail rails, 24×7 RTGS and UPI-led innovation is considered a global benchmark.

Challenges and Criticisms

Despite reforms, friction remains. Smaller cooperative and rural banks sometimes lag in onboarding 24×7 NEFT and RTGS, so customers face occasional delays late at night or during system upgrades. Settlement failures, though rare, continue to occur. The RBI has strengthened the Turn Around Time (TAT) framework to mandate auto-reversal of failed transactions with penal interest, but consumer awareness of grievance redress remains patchy.

Cybersecurity is the other area of concern. Phishing attacks, social engineering around SWIFT-NEFT workflows and fake RTGS confirmation messages have led to significant fraud. The RBI’s Digital Payments Intelligence Platform and the proposed sector-wide fraud registry aim to close these gaps. Small businesses also report that NEFT processing delays in batches can disrupt working capital planning when compared with instant UPI or IMPS transfers.

From a policy standpoint, NEFT and RTGS coexist with newer NPCI rails. Critics argue that the dual-rail system creates confusion for retail users who may not know when to choose which. The RBI’s response is that wholesale and retail needs are genuinely different and that giving customers optionality strengthens resilience.

Prelims Pointers

- NEFT stands for National Electronic Funds Transfer

- RTGS stands for Real Time Gross Settlement

- Both are owned and operated by the Reserve Bank of India

- NEFT settles in half-hourly batches on a deferred net basis

- RTGS settles every transaction individually in real time on a gross basis

- RTGS minimum amount is Rs 2 lakh; NEFT has no minimum

- NEFT became 24×7 on 16 December 2019

- RTGS became 24×7 on 14 December 2020

- Online NEFT and RTGS are free for savings account holders since 1 January 2020

- Legal framework: Payment and Settlement Systems Act, 2007

- IMPS and UPI are run by NPCI, not by the RBI

- The RBI Digital Payments Index is the official adoption tracker

Mains Practice Questions

Q1. “Payments infrastructure has become a strategic public good in India.” Discuss the role of NEFT, RTGS and UPI in the transformation of the Indian financial system. (250 words)

- Map wholesale (RTGS) and retail (NEFT, IMPS, UPI) rails

- Highlight 24×7 operations, zero charges for savings customers and JAM trinity

- Address resilience, cybersecurity and financial inclusion outcomes

Q2. Explain the key differences between NEFT and RTGS. How does their coexistence support financial inclusion and economic efficiency? (150 words)

- Contrast settlement type, limits, timings and charges

- Link NEFT to retail salary and DBT flows and RTGS to corporate and treasury flows

- Conclude with RBI’s role in maintaining both systems as public digital infrastructure

Conclusion

Understanding neft meaning is a starting point, not an end. NEFT and RTGS are two complementary arteries of the Indian banking system, designed by the RBI to move both everyday and high-value funds reliably. Their coexistence with NPCI rails such as IMPS and UPI has given India a uniquely deep payments stack, one that has been exported as a model through initiatives like UPI linkages with Singapore, France and the UAE.

For the civil services aspirant, these payment rails are a reminder that financial infrastructure is policy infrastructure. Command over the NEFT vs RTGS distinction, the transaction limits and the 24×7 timings equips you to engage with GS3 Economy questions on digital public goods, financial inclusion and the RBI’s evolving stewardship of the payments ecosystem.

Frequently Asked Questions

What is NEFT meaning in banking?

NEFT stands for National Electronic Funds Transfer. It is a nationwide centralised payment system owned and operated by the Reserve Bank of India that allows bank-to-bank transfers on a deferred net settlement basis. NEFT became 24x7x365 on 16 December 2019 and charges nothing for online transactions initiated by savings account customers.

Why is NEFT important for UPSC aspirants?

NEFT appears in GS3 Economy questions on banking, digital public infrastructure and financial inclusion. Aspirants must know its RBI ownership, 24×7 availability, deferred net settlement design and zero-charge regime. It is also a staple in RBI Grade B, SSC and state PSC exams, and in general-awareness sections of banking recruitments.

How is NEFT related to RTGS?

Both NEFT and RTGS are RBI-run bank-to-bank payment systems, but they serve different needs. NEFT uses deferred net settlement in half-hourly batches and has no minimum amount. RTGS, or Real Time Gross Settlement, settles each transaction individually in real time and requires a minimum of Rs 2 lakh. Together they cover retail and wholesale flows.

What is the minimum and maximum amount for NEFT?

NEFT has no RBI-prescribed minimum or maximum amount. Individual banks may set per-transaction or daily caps for internet and mobile banking, usually up to Rs 10 lakh or Rs 25 lakh for retail customers. Branch-initiated NEFTs typically carry higher limits subject to KYC and relationship size.

Are NEFT transactions free?

Yes for most users. The RBI abolished processing charges on online NEFT and RTGS for savings bank customers from 1 January 2020 to promote digital payments. Banks may still levy capped fees for branch-originated NEFT: up to Rs 2.50 plus GST for amounts up to Rs 10,000 and up to Rs 25 plus GST above Rs 2 lakh.

What is the difference between NEFT and UPI?

NEFT is an RBI-run batch settlement rail primarily used via net banking or branches for bank-to-bank transfers of any size. UPI, run by NPCI, is a mobile-first, instant, 24×7 interface layered on IMPS with a typical per-transaction cap of Rs 1 lakh. NEFT suits salary and vendor payments; UPI dominates retail peer-to-peer flows.

How long does an NEFT transfer take?

Because NEFT settles 24x7x365 in 48 half-hourly batches starting at 00:30, most transfers credit within 30 minutes to two hours. Banks usually reflect credit in the beneficiary account within the same batch cycle. If a transfer is not credited within two hours, the remitter can seek auto-reversal under the RBI Turn Around Time framework.

What is the legal framework governing NEFT and RTGS?

Both systems operate under the Payment and Settlement Systems Act, 2007, which empowers the Reserve Bank of India to authorise, regulate and supervise payment systems in India. The RBI issues master directions on NEFT and RTGS participation, grievance redress, settlement timings and charges, and audits them annually as systemically important payment systems.