Introduction

The reverse repo rate is one of the most frequently asked and most misunderstood concepts in Indian monetary policy. In plain terms, it is the interest the Reserve Bank of India pays to commercial banks when they park their surplus money with it overnight. For the UPSC aspirant, the rate matters because it anchors the lower boundary of the policy corridor, signals the RBI’s liquidity stance and directly influences short-term interest rates across the banking system.

From 2020 onwards the operational importance of the reverse repo rate has changed. The RBI introduced the Standing Deposit Facility (SDF) in April 2022, which in effect replaced the fixed-rate reverse repo as the floor of the liquidity adjustment facility corridor. Understanding both the historical role and the current position of the reverse repo rate is essential for GS3 Economy and for interpreting current affairs items on monetary policy announcements.

Quick Facts at a Glance

| Attribute | Detail |

|---|---|

| Definition | Rate at which RBI borrows from commercial banks against government securities |

| Instrument type | Liquidity Adjustment Facility (LAF) tool |

| Current status | Fixed reverse repo retained symbolically at 3.35%, SDF is effective floor |

| SDF rate | 25 basis points below repo rate (as of April 2026) |

| Collateral | Government securities (repo); none for SDF |

| Tenor | Overnight (most common) |

| Legal basis | RBI Act 1934, section 17 |

| Decided by | Monetary Policy Committee (MPC) |

Background and Historical Context

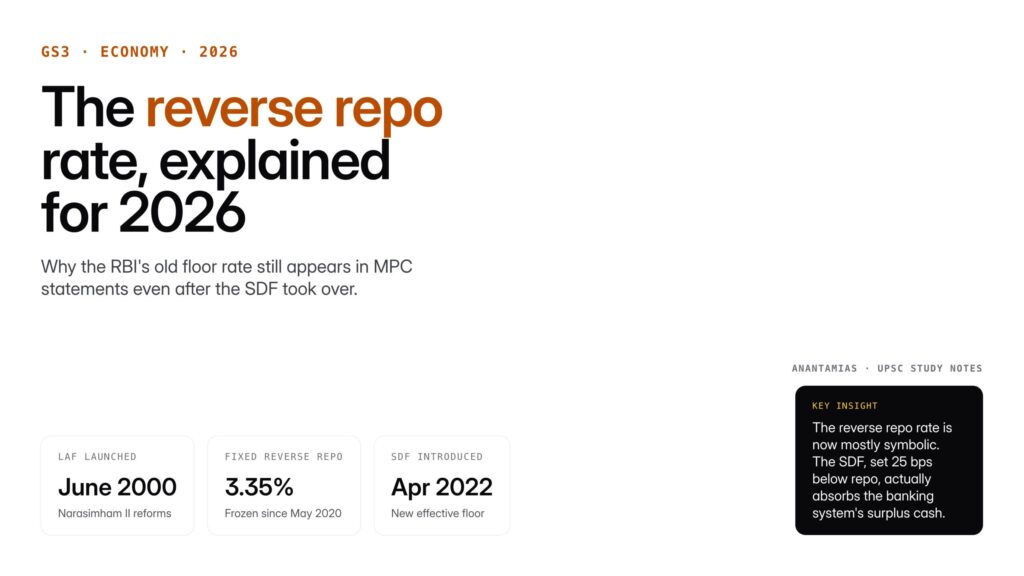

The Liquidity Adjustment Facility (LAF) was introduced in June 2000 on the recommendations of the Narasimham Committee II (1998) to modernise Indian monetary operations. LAF gave the RBI two symmetric instruments, the repo and the reverse repo, to inject or absorb liquidity on an overnight basis. Before LAF, open market operations and statutory ratios like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) were the main levers, which were blunter and slower.

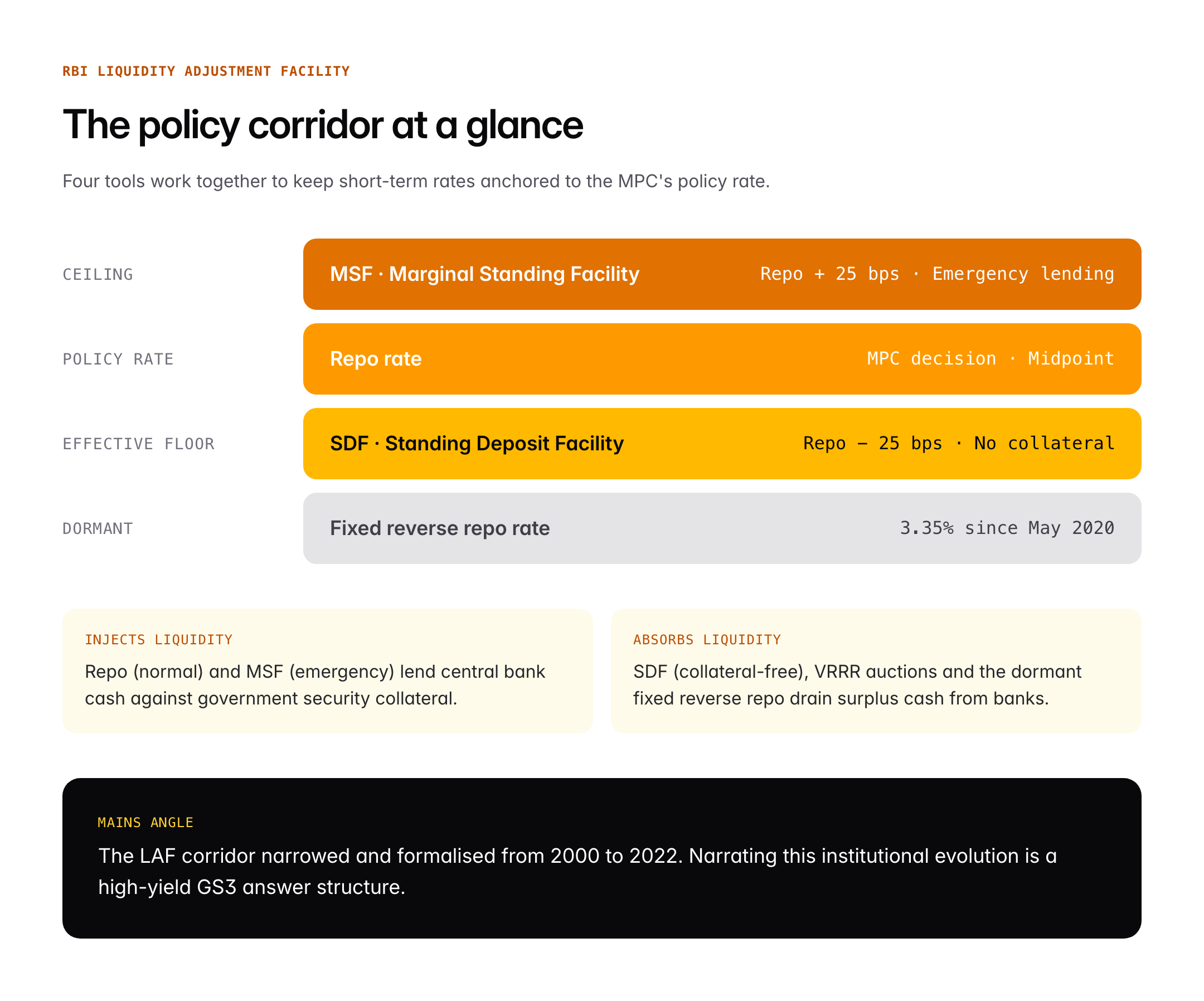

In the early years of LAF the repo and reverse repo rates were independently set, but from 2004 onwards the RBI moved toward a corridor framework. Under this framework the repo rate became the single policy rate and the reverse repo rate became a derived rate, typically kept 25 to 100 basis points below the repo. The Marginal Standing Facility (MSF), introduced in 2011, became the upper ceiling of the corridor, usually 25 basis points above the repo.

The 2014 Urjit Patel Committee report formalised the flexible inflation targeting framework, anchoring the MPC’s policy around a 4 percent CPI inflation target with a plus-or-minus 2 percent tolerance band. The reverse repo rate was always subordinate to the repo rate under this framework, but during the Covid-19 pandemic it became operationally decoupled: the repo was cut to 4.00 percent while the reverse repo was cut further to 3.35 percent to push banks to lend rather than park funds.

The asymmetric widening of the corridor created policy noise. The April 2022 introduction of the Standing Deposit Facility (SDF) resolved this. The SDF accepts deposits from banks without collateral, unlike reverse repo, and now serves as the effective floor of the LAF corridor. The fixed reverse repo rate remains in the RBI’s toolkit but is largely inactive.

Key Features of the Reverse Repo Rate

Mechanism

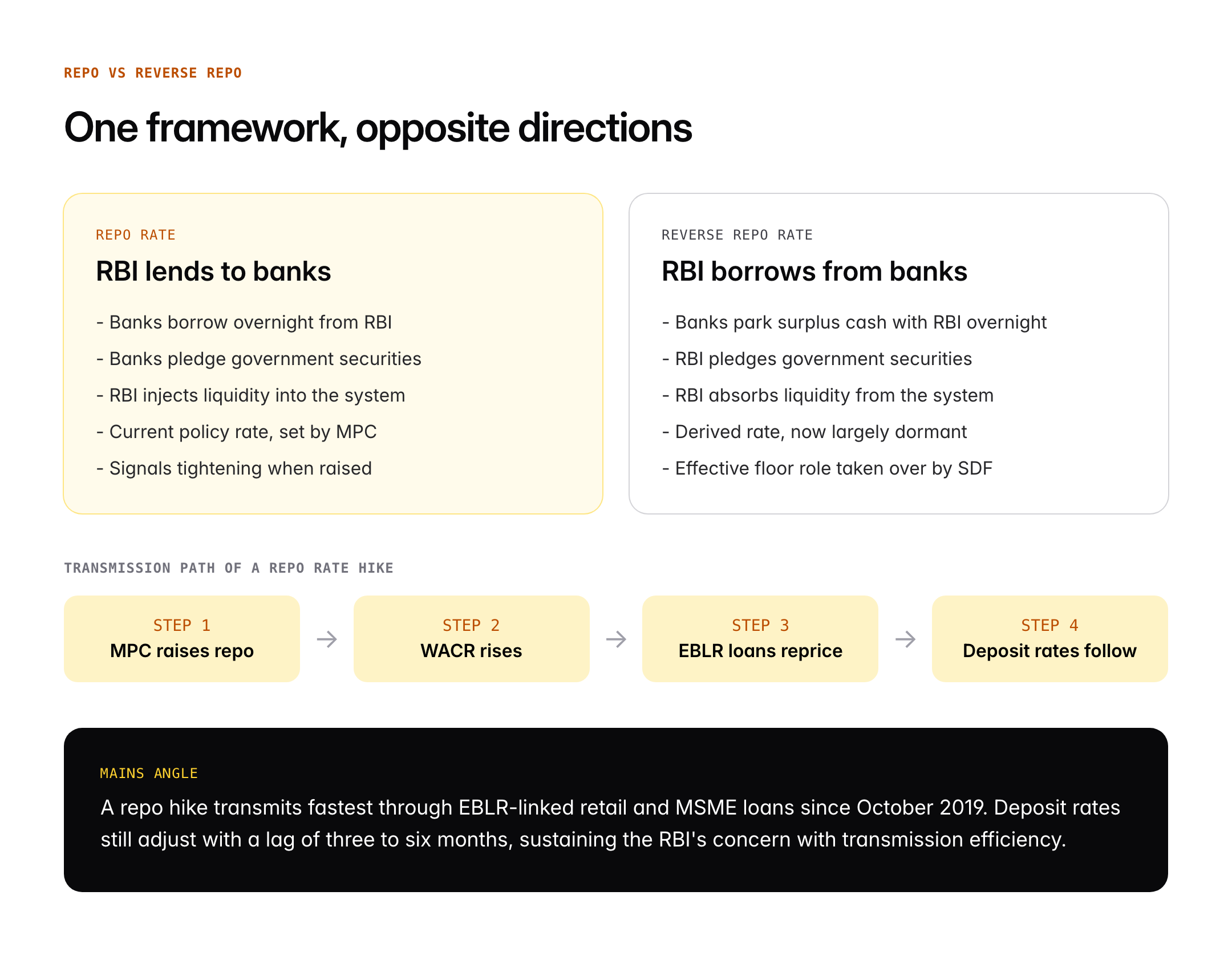

Under a reverse repo transaction, a commercial bank with surplus cash lends it to the RBI overnight and receives government securities as collateral. The next morning the transaction reverses: the RBI returns the cash plus interest at the reverse repo rate, and the bank returns the securities. From the RBI’s perspective, this absorbs liquidity from the system; from the bank’s perspective, it is a safe overnight deposit.

Corridor Position

The LAF corridor has three tiers, from floor to ceiling:

- SDF rate (floor): 25 basis points below repo; collateral-free RBI deposit.

- Repo rate (policy rate): the midpoint that the MPC sets.

- MSF rate (ceiling): 25 basis points above repo; emergency lending window for banks.

The fixed reverse repo rate sits within or below this corridor but no longer binds market behaviour.

Variable Rate Reverse Repo (VRRR)

In addition to the fixed-rate instrument, the RBI conducts Variable Rate Reverse Repo auctions. Banks bid rates to deposit funds with the RBI for tenors ranging from 1 to 28 days. This is the active liquidity-absorption tool during surplus-liquidity phases. In FY 2023-24 the VRRR absorbed amounts up to 3 lakh crore rupees on peak days.

Signalling Function

Even when operationally dormant, the reverse repo rate retains a signalling role. A cut conveys that the RBI wants banks to lend more and hold less idle cash; a hike signals the opposite. During the 2020 to 2022 accommodative phase, the RBI used reverse repo adjustments as a soft signal distinct from repo rate moves, maintaining optionality.

Relationship with Inflation Targeting

The reverse repo rate connects to flexible inflation targeting indirectly. By influencing short-term money-market rates through the corridor, it affects weighted average call money rate (WACR), which the RBI treats as the operational target of monetary policy. When WACR is close to the repo rate, transmission is considered effective.

Significance for UPSC and General Knowledge

- Core GS3 Economy topic on monetary policy instruments; frequently asked in Prelims as one-mark factual question.

- Case study of institutional evolution: LAF (2000), corridor framework (2004), MSF (2011), SDF (2022).

- Connects to financial stability since it manages the call money rate volatility.

- Illustrates RBI Act 1934 section 17 powers on rediscounting and lending.

- Useful for analysing the policy response to the Covid-19 pandemic and subsequent inflation surge.

- Links to fiscal-monetary coordination through the government securities collateral requirement.

Detailed Analysis: Monetary Transmission and Impact

Effective monetary policy transmission is the chain from policy rate to deposit rates, lending rates and finally aggregate demand and inflation. The reverse repo rate historically influenced this chain at its very first link: by setting the opportunity cost of idle bank balances, it shaped the floor below which overnight interbank rates could not sustainably fall.

During FY 2022-23 and FY 2023-24, the RBI raised the repo rate from 4.00 percent to 6.50 percent cumulatively. Under the new framework, the SDF rose in parallel from 3.75 percent to 6.25 percent. The fixed reverse repo stayed at 3.35 percent, frozen as a dormant artefact. WACR tracked the repo rate closely, suggesting transmission was effective under the SDF-anchored corridor.

The banking sector impact runs through two channels. First, the return on banks’ surplus liquidity is set by the SDF, so when SDF rises banks earn more on parked funds and have less incentive to lend at very low rates. Second, banks’ marginal cost of funds-based lending rate (MCLR) and external benchmark-linked lending rate (EBLR) eventually reflect the policy rate. Home loans linked to the repo rate externally respond within a few months; deposit rates adjust with a lag.

Borrower impact depends on which instrument a loan is linked to. Since October 2019, all new floating-rate retail and MSME loans must be linked to an external benchmark, typically the RBI repo rate. A 25 basis point repo hike therefore flows quickly to EMIs. The reverse repo rate no longer has a direct borrower impact, though it continues to be referenced in media coverage.

Fiscal implications matter too. High reverse repo absorption by RBI effectively locks government-security collateral with banks, reducing the free float. This can shift yield curves and affect central-government borrowing costs. During the 2020 to 2022 period, large LAF surplus parking at reverse repo kept the 10-year G-sec yield around 6 percent despite rising inflation expectations, illustrating the complex interaction between liquidity management and term premia.

Comparative Perspective

| Feature | Reverse Repo | Repo Rate | SDF | MSF |

|---|---|---|---|---|

| Direction | RBI absorbs liquidity | RBI injects liquidity | RBI absorbs liquidity | RBI injects liquidity |

| Collateral | Govt securities from RBI | Govt securities from banks | None | Govt securities from banks |

| Corridor position | Historic floor, now dormant | Policy rate (mid) | Effective floor | Ceiling |

| Tenor | Overnight | Overnight | Overnight | Overnight |

| Current status | Frozen at 3.35% | 6.50% (illustrative) | 6.25% | 6.75% |

Internationally, the US Federal Reserve’s Overnight Reverse Repurchase Facility and the European Central Bank’s deposit facility rate play equivalent floor roles. The Bank of England’s corridor is structured differently but the principle is similar: a floor instrument to cap overnight rate declines.

Challenges and Criticisms

Critics of the historical reverse repo structure argued it was collateral-constrained: the RBI’s available government securities limited how much liquidity could be absorbed, which became binding during large capital inflow episodes. The SDF resolves this by removing the collateral requirement.

A second critique concerns signalling confusion. During the 2020 to 2022 phase when the RBI kept the fixed reverse repo below the repo by a widening gap, market participants found it difficult to interpret the effective policy stance. The April 2022 SDF introduction and the subsequent dormancy of the fixed reverse repo have simplified communication.

A third concern is transmission lags. Even when the corridor is clear, deposit rate adjustments take three to six months, and MCLR-linked loans often longer. The RBI has repeatedly urged banks to pass on rate changes promptly, and the shift to EBLR from 2019 was designed to address this.

Finally, some economists argue that absorption tools like reverse repo and SDF may be insufficient during structural surplus phases driven by forex intervention or large government cash balances. Open market sales of securities and CRR adjustments remain complementary tools.

Prelims Pointers

- The Liquidity Adjustment Facility was introduced in June 2000 on the Narasimham Committee II’s recommendation.

- The Marginal Standing Facility was introduced in May 2011 as the corridor ceiling.

- The Standing Deposit Facility was operationalised on 8 April 2022.

- The SDF is collateral-free, unlike the reverse repo.

- The MPC was constituted under the amended RBI Act in 2016.

- The flexible inflation targeting target is 4 percent CPI with a plus-or-minus 2 percent band.

- The fixed reverse repo rate has been retained at 3.35 percent since May 2020.

- The reverse repo collateral is drawn from RBI’s government securities portfolio.

- The Weighted Average Call Money Rate is the operational target of monetary policy.

- Variable Rate Reverse Repo auctions typically run for 1 to 28 days.

- External Benchmark Lending Rate for new retail and MSME floating loans is mandatory from October 2019.

- The RBI’s Monetary Policy Department conducts LAF operations through e-Kuber platform.

Mains Practice Questions

- Discuss how the introduction of the Standing Deposit Facility in April 2022 has altered India’s monetary policy corridor and the relevance of the fixed reverse repo rate.

- Explain the LAF corridor before SDF (floor = reverse repo with collateral constraint).

- Detail SDF: collateral-free absorption, 25 basis points below repo.

- Assess consequences: clearer signalling, effective floor, dormant fixed reverse repo, improved transmission.

- “Monetary policy transmission in India remains uneven despite successive reforms of the Liquidity Adjustment Facility.” Critically examine.

- Reforms: LAF 2000, corridor 2004, MSF 2011, MPC 2016, SDF 2022, EBLR 2019.

- Evidence of transmission: WACR tracking repo, faster EBLR-linked loan adjustments.

- Remaining gaps: deposit rate lags, MCLR legacy loans, surplus-liquidity phases, bank-level variation.

Conclusion

The reverse repo rate has travelled a long distance from being the active floor of Indian monetary operations to becoming a largely symbolic rate maintained at 3.35 percent while the Standing Deposit Facility does the real work of absorbing surplus liquidity. Understanding this evolution is essential for anyone interpreting an MPC announcement or a financial-press headline that still uses the term reverse repo.

For UPSC aspirants, the learning is twofold. First, recognise the institutional layering from LAF to MSF to SDF as a mature central bank’s response to operational constraints. Second, use the corridor framework to answer Mains questions on monetary transmission, financial stability and the interaction between fiscal and monetary policy. The reverse repo rate today is a reminder that policy instruments can live on long after their operational role has been handed to a successor.

Frequently Asked Questions

What is the reverse repo rate?

The reverse repo rate is the interest rate at which the Reserve Bank of India borrows surplus funds overnight from commercial banks against government securities as collateral. It is part of the Liquidity Adjustment Facility and historically served as the floor of the LAF corridor, absorbing excess liquidity from the banking system to support RBI’s monetary policy stance.

Why is the reverse repo rate important for UPSC aspirants?

The reverse repo rate is a core GS3 Economy topic covering monetary policy tools, RBI’s LAF framework and the evolution from LAF to SDF. Prelims questions often test the current rate and the agency that sets it, while Mains questions explore transmission mechanisms, corridor design and the policy response to events like the Covid-19 pandemic and subsequent inflation surge.

How is reverse repo rate different from repo rate?

The repo rate is what RBI charges when it lends to banks against government securities, injecting liquidity; the reverse repo rate is what RBI pays when it borrows from banks, absorbing liquidity. The repo is the policy rate set by the MPC, while the reverse repo has historically been a derived rate kept at a lower level within the LAF corridor.

What is the current status of the reverse repo rate in India?

The fixed reverse repo rate has been retained at 3.35 percent since May 2020 but is largely dormant operationally. Since April 2022, the Standing Deposit Facility (SDF), set 25 basis points below the repo rate, has served as the effective floor of the LAF corridor. The RBI uses Variable Rate Reverse Repo auctions as the active liquidity-absorption tool.

How does the reverse repo rate affect borrowers?

The reverse repo rate no longer has a direct impact on retail borrowers, as most new floating-rate retail and MSME loans since October 2019 are linked to the repo rate through the External Benchmark Lending Rate framework. Historically, a higher reverse repo made parking surplus cash more attractive to banks, which could indirectly nudge deposit and lending rates upward.

What is the Standing Deposit Facility and how is it related?

The Standing Deposit Facility (SDF), operationalised on 8 April 2022, allows banks to deposit surplus cash with the RBI overnight without any collateral, at a rate 25 basis points below the repo rate. It replaced the fixed reverse repo as the effective floor of the LAF corridor and resolved the historic collateral constraint of the reverse repo instrument.

Who decides the reverse repo rate?

The Monetary Policy Committee (MPC), constituted under the amended RBI Act in 2016, sets the repo rate. The reverse repo, SDF and MSF rates are derived from the repo rate based on the corridor width announced by the RBI. The MPC meets at least six times a year, and the RBI Governor chairs the six-member committee with a casting vote.

How does reverse repo relate to flexible inflation targeting?

Flexible inflation targeting, formalised in 2016, sets a 4 percent CPI inflation target with a plus-or-minus 2 percent tolerance band. The MPC raises or lowers the repo rate to keep inflation within the band, and the reverse repo and SDF follow mechanically. Effective transmission through the corridor keeps the Weighted Average Call Money Rate close to the repo, supporting the inflation target.