Why in News?

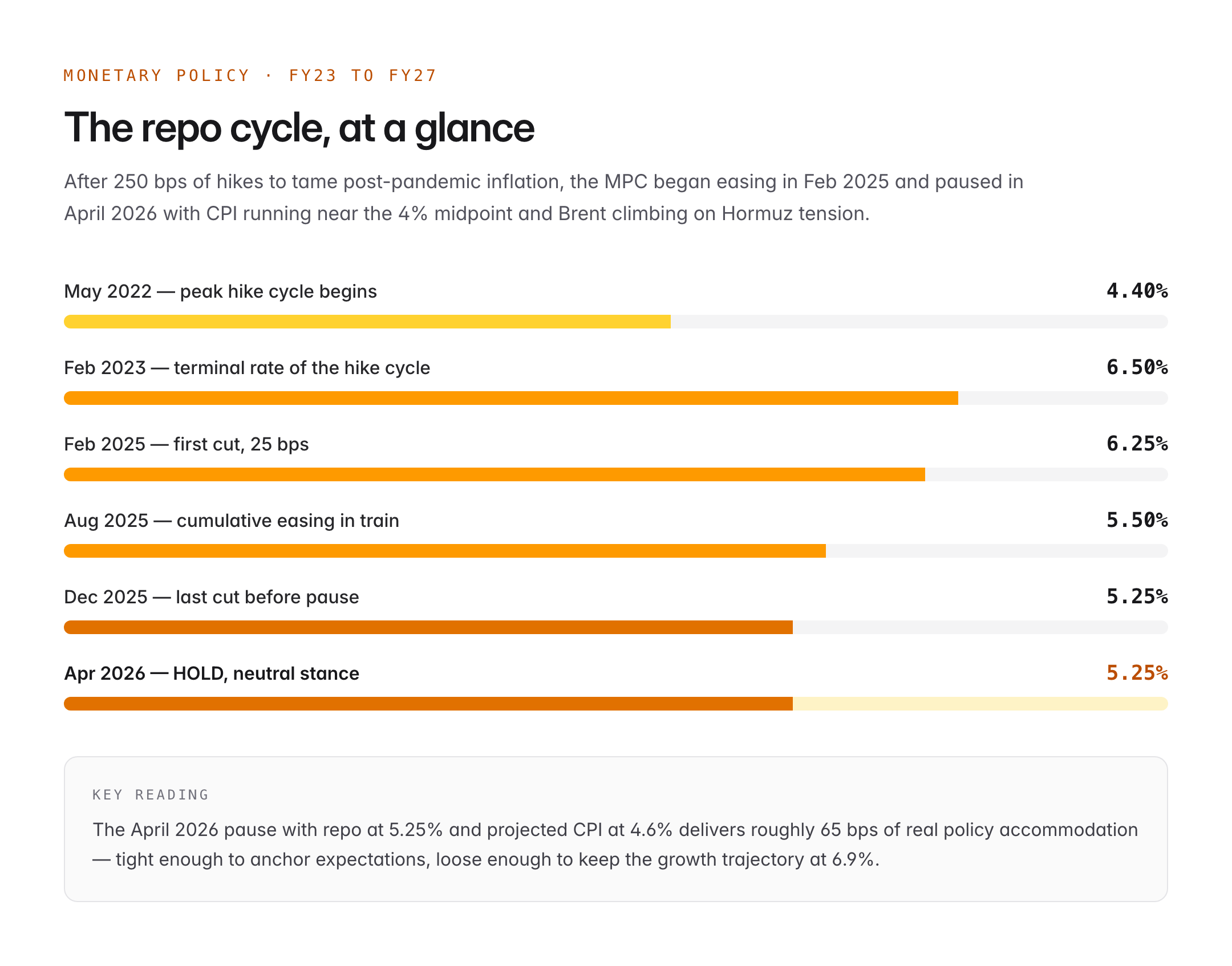

On 10 April 2026, the Reserve Bank of India’s Monetary Policy Committee (MPC) concluded its first bi-monthly review of FY27 by holding the policy repo rate at 5.25 per cent. Governor Sanjay Malhotra announced that all six members voted to retain the neutral stance first adopted in October 2024, signalling a calibrated pause after the 25 basis point cut delivered in December 2025.

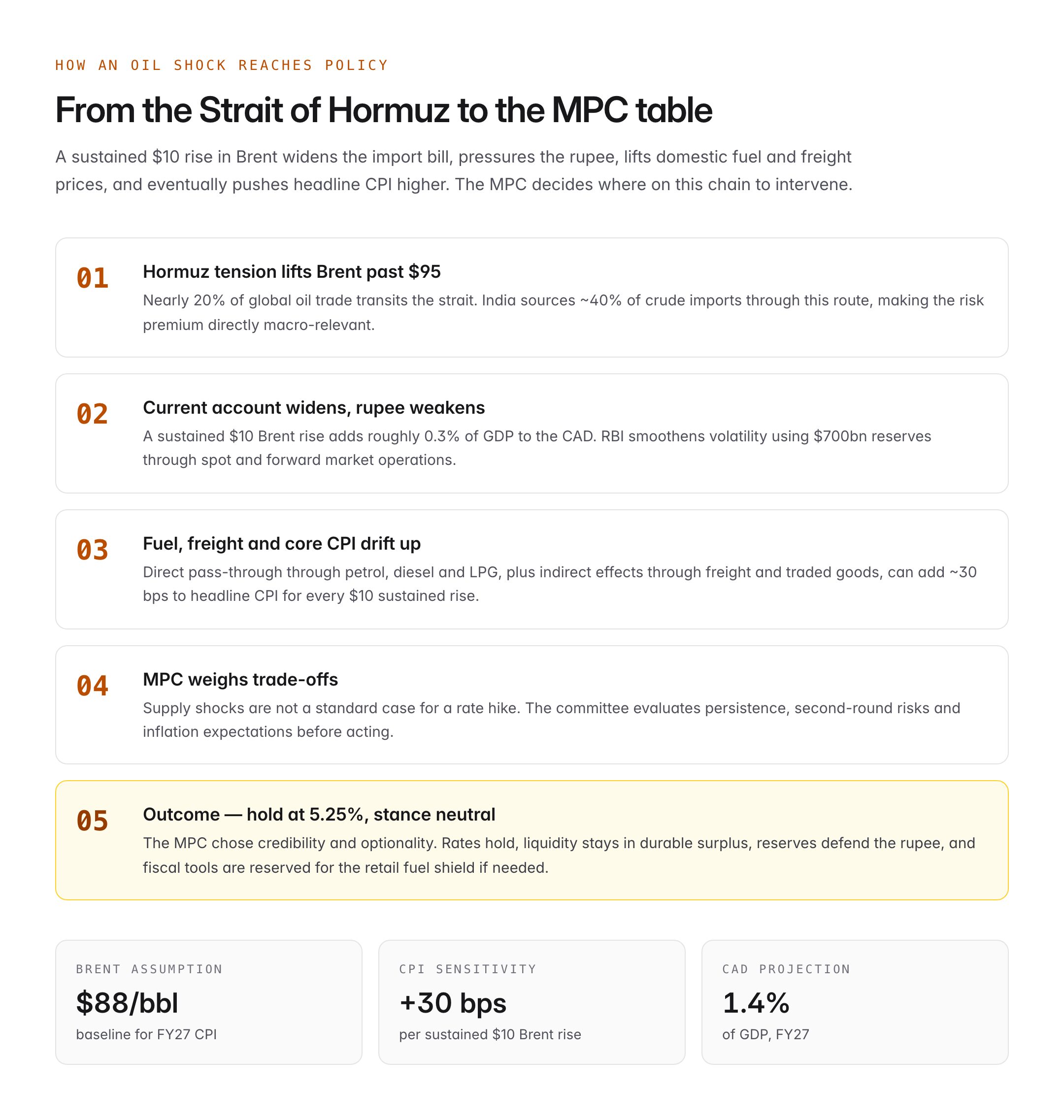

The decision was taken against a sharp external backdrop. Escalating tensions around the Strait of Hormuz, triggered by the latest round of West Asia hostilities, had pushed Brent crude past 95 dollars a barrel in the week before the meeting. Despite this imported inflation risk, the MPC retained its CPI forecast close to the midpoint of the tolerance band and nudged its growth projection higher.

The review matters because it reveals how the RBI is navigating a textbook supply shock while protecting a disinflation record that took three years to build. The repo pause, the neutral stance, and the unchanged liquidity tools together outline India’s policy choreography when domestic conditions are comfortable but the external environment is not.

UPSC Relevance at a Glance

| Dimension | Detail |

|---|---|

| GS Paper | GS3 — Indian Economy, Monetary Policy, Inflation |

| Prelims | MPC composition, MPFA 2015, RBI Act Section 45ZA, LAF corridor, SDF, MSF, CRR, flexible inflation targeting |

| Mains | Monetary transmission, crude-CAD linkage, stance vs rate distinction, rupee defence, policy trade-offs |

| Syllabus Tags | Indian Economy, External Sector, Banking Regulation, Energy Security |

Background and Context

India’s monetary policy architecture was fundamentally restructured in 2015-16. The Monetary Policy Framework Agreement (MPFA) signed between the Government of India and the RBI in February 2015 formally adopted a flexible inflation targeting (FIT) regime. This was given statutory backing through the amended Reserve Bank of India Act, 1934. Section 45ZA of the Act empowers the central government, in consultation with the RBI, to set the inflation target once every five years.

The current target, notified for 2021-2026 and extended into the new five-year cycle, is headline Consumer Price Index (CPI) inflation of 4 per cent with a tolerance band of plus or minus 2 percentage points. A failure to keep CPI within 2-6 per cent for three consecutive quarters triggers a statutory report from the RBI to Parliament explaining the miss and proposing remedial action.

Policy decisions are taken by the Monetary Policy Committee, a six-member statutory body constituted under Section 45ZB. It has three RBI members, the Governor who chairs it, a Deputy Governor in charge of monetary policy, and one officer nominated by the central board, and three external members appointed by the central government for a non-renewable four-year term. Decisions are taken by majority vote; the Governor holds a casting vote in the event of a tie.

The operating framework rests on the Liquidity Adjustment Facility (LAF) corridor. The repo rate is the policy rate at which banks borrow overnight from the RBI against government securities. The Standing Deposit Facility (SDF), introduced in April 2022, forms the floor of the corridor and absorbs surplus liquidity without collateral. The Marginal Standing Facility (MSF) is the ceiling, 25 basis points above the repo rate, allowing banks to draw emergency liquidity against statutory liquidity ratio (SLR) securities. A symmetric corridor of plus or minus 25 basis points around the repo has been the norm since April 2022.

Between May 2022 and February 2023, the MPC raised the repo by 250 basis points to 6.50 per cent to break a post-pandemic inflation surge. A first cut of 25 basis points in February 2025 began the easing cycle, followed by further cuts that brought the repo down to 5.50 per cent, and a 25 basis point reduction in December 2025 took it to 5.25 per cent. The April 2026 review was therefore the first pause of the current cycle.

Key Features of the April 2026 Review

Rate Action and Stance

The MPC voted six to zero to hold the repo rate at 5.25 per cent. The SDF stayed at 5.00 per cent and the MSF at 5.50 per cent, preserving the symmetric 25 basis point corridor. The Bank Rate was aligned with the MSF. The cash reserve ratio (CRR) was left untouched at 4 per cent of net demand and time liabilities, and the SLR was unchanged at 18 per cent.

The stance remained neutral, language that permits the committee to move in either direction depending on incoming data. Governor Malhotra underlined that a neutral stance is not a tightening bias in disguise; it is an acknowledgement that the policy rate is close to what the committee considers the effective real rate consistent with the 4 per cent CPI objective.

Growth and Inflation Projections

The RBI revised its real GDP growth projection for FY27 to 6.9 per cent, up 10 basis points from the February print, with quarterly trajectory of 7.1, 7.0, 6.8 and 6.7 per cent. The upward revision reflected stronger rural demand, a robust services PMI, and a favourable base effect in the first half.

Headline CPI inflation for FY27 is projected at 4.6 per cent, with Q1 at 4.8, Q2 at 4.7, Q3 at 4.5 and Q4 at 4.4 per cent. The committee assumed a normal southwest monsoon, a fiscal pass-through of recent excise cuts on transport fuels, and an average Brent price of 88 dollars a barrel for the full year. The Governor flagged that every 10 dollar sustained rise in Brent beyond the baseline would add roughly 30 basis points to headline CPI through direct fuel and indirect transport, freight and core goods channels.

External Environment and Rupee Defence

The West Asia flare-up around the Strait of Hormuz, through which nearly a fifth of global oil trade passes, has been the dominant external story. India sources close to 40 per cent of its crude imports through the strait. The Governor confirmed that the RBI had intervened in both spot and forward segments to smooth rupee volatility, without defending any particular level.

Forex reserves stood at around 700 billion dollars, comfortably over 11 months of import cover. The Governor argued that reserves adequacy, combined with a current account deficit projected at 1.4 per cent of GDP, gave India a shock-absorbing buffer that was absent during the 2013 taper tantrum.

Transmission and Liquidity

The Governor noted that the 125 basis points of cumulative easing since February 2025 had transmitted fully to the weighted average lending rate on fresh rupee loans, with a pass-through of about 90 basis points to the outstanding book. Loans linked to the external benchmark lending rate (EBLR) adjusted almost immediately, while marginal cost of funds based lending rate (MCLR) loans moved with a lag of one to two quarters. System liquidity had shifted to a durable surplus of around 1.8 lakh crore rupees, and the RBI would continue to use variable rate repo and reverse repo auctions as the primary tools of fine-tuning.

Significance

- The pause signals that India’s disinflation is durable enough to withstand a classic supply shock without a premature move either way, preserving MPC credibility at a delicate juncture.

- A neutral stance keeps option value open; if the Hormuz premium on oil proves sticky, the committee can pivot without a fresh stance change that would disturb bond markets.

- The unchanged CRR and the durable liquidity surplus indicate that the RBI is willing to separate price policy from quantity policy, allowing banks to lend while the policy rate holds the inflation line.

- Full EBLR transmission and improved MCLR pass-through validate the reforms begun with the October 2019 external benchmark directive, which forced banks off opaque internal benchmarks.

- A 6.9 per cent growth projection, among the highest in the G20, reinforces India’s macro narrative at a time when global financial conditions have tightened on the back of oil and a firmer dollar.

- Robust forex reserves and a moderate current account deficit allow the central bank to calibrate rupee smoothing without depleting buffers, a clear contrast with past crude-driven episodes in 2011-13 and 2018.

Concerns and Challenges

The Hormuz risk is not fully priced in. If tensions escalate to actual disruption rather than the current sentiment premium, Brent could touch 110-120 dollars, and India’s CPI could breach 5.5 per cent by late FY27, testing the upper bound of the tolerance band and the MPC’s neutral posture.

Food inflation remains the volatile swing factor. Vegetable price spikes have repeatedly pushed headline above core in recent cycles, and the RBI’s ability to look through transient supply-side shocks is tested each time. A deficient monsoon or unseasonal rainfall could quickly nullify the favourable assumption built into the projections.

The transmission story, while improved, is uneven across borrower categories. Deposit rates have lagged, squeezing bank margins and creating political pressure on savers, particularly senior citizens who rely on term deposit income. The shift to floating-rate retail loans has also amplified household sensitivity to any future tightening.

There is an intellectual debate about the real neutral rate. Some committee members and external economists argue that India’s neutral real rate has risen with the growth acceleration and that holding rates at 5.25 per cent with projected CPI at 4.6 per cent delivers only 65 basis points of real accommodation, which is too tight for a 7 per cent growth economy. Others counter that the neutral rate must be calibrated to medium-term inflation expectations, not realised inflation.

Global spillovers remain the deeper constraint. The US Federal Reserve’s pause and the narrower interest differential have reduced the room for unilateral Indian easing without triggering rupee pressure. Coordinating domestic objectives with external stability is the structural tension the MPC will keep navigating.

Comparative / Historical Perspective

Two earlier crude-driven episodes offer useful reference points. In 2011-12, an oil spike to 120 dollars under an opaque multiple-indicator regime led to a disorderly rate cycle and double-digit CPI. In 2018, Brent touched 86 dollars and the RBI hiked by 50 basis points under a fledgling FIT framework; the rupee still fell to 74 per dollar. The April 2026 posture is materially different because of the institutional buffers now in place.

| Episode | Trigger | RBI Response | CPI Peak | INR Pressure |

|---|---|---|---|---|

| 2011-12 | Brent > 120, fiscal slippage | Rate hikes, disorderly liquidity | 10.9% | Rupee to 57 |

| 2018 | Brent > 86, EM selloff | 50 bps hikes, FX intervention | 5.1% | Rupee to 74 |

| 2022 | War shock, 8.0% CPI | 250 bps hike over 10 months | 7.8% | Rupee to 83 |

| April 2026 | Hormuz tension, Brent 95 | Hold, neutral stance | 4.6% proj | Orderly, managed |

The shift from reactive hikes to a confident hold reflects the maturing of the FIT regime, deeper reserves, and a more credible MPC communication framework.

Way Forward

- The Ministry of Finance should use the fiscal space opened by strong tax buoyancy to cushion any sustained Brent overshoot through calibrated excise adjustments on petrol and diesel, limiting second-round effects on core CPI.

- The RBI should publish a technical note on its estimate of the neutral real rate to anchor market expectations and reduce speculation about implicit policy biases.

- The Department of Economic Affairs and the RBI should accelerate the operationalisation of rupee settlement arrangements for West Asian crude, reducing dollar demand in the trade channel during periods of geopolitical stress.

- The Department of Food and Public Distribution, in coordination with the Ministry of Agriculture, should strengthen buffer management for tomato, onion and pulses to reduce the high-frequency food inflation volatility that repeatedly distorts headline CPI.

- The Indian Banks Association and scheduled commercial banks should accelerate deposit-rate rationalisation to preserve savings incentives and widen the pool of small deposits that remain sticky across rate cycles.

- The Petroleum Ministry should expand the Strategic Petroleum Reserve from the current 5.3 million tonnes at Visakhapatnam, Mangalore and Padur to the sanctioned Phase II volumes at Chandikhol and Padur, delivering at least 22 days of national import cover by 2028.

- SEBI and the RBI should jointly deepen the corporate bond market so that monetary transmission is not routed exclusively through bank balance sheets, distributing interest rate risk more efficiently.

Conclusion

The April 2026 review is a compact case study in how a mature inflation-targeting regime should respond to an imported supply shock. By holding the repo at 5.25 per cent, retaining a neutral stance, and keeping the LAF corridor and CRR unchanged, the MPC has chosen credibility over cleverness. It has allowed the disinflation dividend of the last three years to do the work of reassuring markets, while preserving the optionality to move in either direction as the Hormuz risk resolves.

For the UPSC aspirant, the decision maps neatly onto the core GS3 syllabus themes of monetary policy, inflation management, external sector resilience and energy security. It also offers a template for essay and ethics-of-governance questions on institutional credibility, rule-based policy, and the value of well-designed statutory frameworks such as the MPFA and Section 45ZA of the RBI Act.

Prelims Pointers

- The repo rate was held at 5.25 per cent in the April 2026 MPC; the stance is neutral.

- The SDF is 5.00 per cent and the MSF is 5.50 per cent, maintaining a symmetric 25 bps LAF corridor.

- CRR is 4.0 per cent and SLR is 18.0 per cent of net demand and time liabilities.

- The FIT target is 4 per cent CPI with a 2-6 per cent tolerance band, under the MPFA 2015.

- Section 45ZA of the RBI Act 1934 empowers the central government, in consultation with RBI, to set the target.

- Section 45ZB constitutes the MPC — six members, three from RBI and three external.

- The Governor has a casting vote; external members serve a four-year non-renewable term.

- SDF was introduced in April 2022 and replaced the fixed-rate reverse repo as the floor of the corridor.

- India’s forex reserves are around 700 billion dollars, covering more than 11 months of imports.

- FY27 real GDP growth projection is 6.9 per cent; CPI projection is 4.6 per cent.

- Brent crude breached 95 dollars a barrel on Hormuz tensions; every 10 dollar sustained rise adds roughly 30 bps to CPI.

- External Benchmark Lending Rate (EBLR) transmission is near full; MCLR transmission works with a lag.

Mains Practice Question

Q. The Reserve Bank of India’s decision to hold the repo rate while retaining a neutral stance, amid an oil shock, illustrates the maturity of India’s flexible inflation targeting framework. Critically examine. (15 marks, 250 words)

- Outline the FIT framework, MPFA 2015, Section 45ZA, MPC composition and LAF corridor; situate the April 2026 pause within the 2022-26 rate cycle.

- Argue the case for maturity, credible disinflation, reserves buffer, smooth transmission, neutral stance optionality, contrast with 2011-12 and 2018 episodes.

- Qualify with limitations, Hormuz tail risk, food volatility, neutral real rate debate, deposit side stress, and global spillovers, and conclude with the institutional design lesson.

Frequently Asked Questions

What is the RBI repo rate after the April 2026 MPC?

The Monetary Policy Committee held the repo rate unchanged at 5.25 per cent in its 10 April 2026 meeting. The Standing Deposit Facility stayed at 5.00 per cent and the Marginal Standing Facility at 5.50 per cent, preserving a symmetric 25 basis point corridor. All six members voted to retain the neutral stance.

Why is the April 2026 RBI monetary policy in news?

The MPC held rates amid a West Asia oil shock, with Brent crude past 95 dollars a barrel on Strait of Hormuz tensions. Governor Sanjay Malhotra announced a pause after the December 2025 cut, revised FY27 GDP up to 6.9 per cent and projected CPI at 4.6 per cent, making this a high-profile test of flexible inflation targeting.

How does this help UPSC preparation?

The review is directly relevant to GS3 on monetary policy, inflation, external sector and energy security. It offers a compact case study linking the MPFA 2015, Section 45ZA of the RBI Act 1934, the MPC’s composition, LAF corridor tools and rupee defence. Prelims can ask factual details; Mains can test policy trade-offs and institutional credibility.

What is the flexible inflation targeting framework?

Flexible inflation targeting is India’s statutory monetary policy regime established by the 2015 Monetary Policy Framework Agreement and Section 45ZA of the amended RBI Act 1934. It sets a headline CPI target of 4 per cent with a 2 to 6 per cent tolerance band. Breaching the band for three consecutive quarters triggers an explanatory RBI report to Parliament.

What is the composition of the Monetary Policy Committee?

The MPC has six members under Section 45ZB of the RBI Act. Three are from the RBI, the Governor as chair, a Deputy Governor in charge of monetary policy and one officer nominated by the central board. Three external members are appointed by the central government for non-renewable four-year terms. Decisions are by majority with the Governor holding a casting vote.

How does a West Asia oil shock affect the Indian economy?

Higher Brent prices widen the current account deficit, pressure the rupee, raise fuel and transport CPI and can seep into core inflation through freight. Every 10 dollar sustained rise adds roughly 30 basis points to India’s headline CPI. India imports nearly 40 per cent of its crude through the Strait of Hormuz, making Hormuz tensions a direct macro risk.

What are SDF, MSF and CRR in monetary policy?

The Standing Deposit Facility is an uncollateralised overnight deposit window for banks at 25 basis points below the repo, forming the corridor floor since April 2022. The Marginal Standing Facility is an overnight window at 25 basis points above the repo, forming the ceiling. The Cash Reserve Ratio is the share of net demand and time liabilities banks must hold as reserves with the RBI, currently 4 per cent.

What is monetary transmission and why does it matter?

Monetary transmission is the process by which changes in the policy repo rate pass through to deposit rates, lending rates such as MCLR and EBLR, bond yields and eventually output and inflation. It matters because policy loosening or tightening only works if banks and markets respond. The RBI reports near-full transmission to EBLR-linked loans and improving MCLR pass-through in the current cycle.